Nestled along the stunning Emerald Coast, Walton County in Florida is renowned for its pristine beaches, charming communities, and a lifestyle that beckons residents and tourists alike. As property values continue to rise in this picturesque region, understanding the nuances of Walton County’s property taxes becomes crucial for homeowners and potential investors. In this blog post, we’ll delve into the essentials of Walton County’s property taxes, shedding light on how they work and offering insights to help you navigate this aspect of real estate ownership.

Understanding the Basics:

Ad Valorem Tax System: Walton County, like many other counties in Florida, employs an ad valorem tax system for property taxation. This means that property taxes are calculated based on the assessed value of the property.

Assessment Process: The Property Appraiser’s Office in Walton County is responsible for determining the assessed value of properties. They consider various factors such as market conditions, property improvements, and recent sales data.

Millage Rates: Property taxes are expressed in terms of millage rates, where one mill is equal to one-tenth of a cent. Walton County’s millage rates are set by local taxing authorities and play a significant role in determining the final property tax amount.

Factors Influencing Property Taxes:

Property Value Trends: The overall trend in property values in Walton County can directly impact your property taxes. Understanding the market dynamics and staying informed about property appreciation is essential.

Homestead Exemption: Florida offers a Homestead Exemption, providing a reduction in the assessed value of a property for primary residents. Walton County residents may qualify for this exemption, leading to a lower property tax bill.

Additional Exemptions: Beyond the Homestead Exemption, there are additional exemptions available in Walton County, such as exemptions for veterans, seniors, and disabled individuals. Exploring these options can provide further relief on property taxes.

Millage Rate Variations: Different areas within Walton County may have varying millage rates based on local needs and services. Being aware of these variations can help you anticipate and plan for property tax expenses.

Payment and Deadlines:

Tax Bills and Notices: Property tax bills are typically mailed out by the Property Appraiser’s Office in November. It’s crucial to carefully review these bills, ensuring accuracy in assessed values and applying any applicable exemptions.

Payment Options: Walton County provides various payment options, including online payments, mail-in options, and in-person payments at designated locations. Familiarizing yourself with these options can streamline the payment process.

Conclusion:

Owning property in Walton County, Florida, comes with the responsibility of managing property taxes. By understanding the assessment process, available exemptions, and payment procedures, homeowners can navigate this aspect of real estate ownership more effectively. Staying informed about local tax policies and seeking professional advice when needed will contribute to a smoother experience in this beautiful corner of the Sunshine State.

In the digital age, where information is readily available at our fingertips, platforms like Zillow have become go-to resources for homeowners, prospective buyers, and real estate enthusiasts. Zillow’s Home Value Zestimate, in particular, is a feature that attempts to provide an estimate of a property’s worth based on various factors. However, as many have experienced, these valuations are not always accurate and can sometimes be significantly off the mark. In this blog post, we’ll delve into the reasons behind the discrepancies and why relying solely on Zillow’s home valuations might not be the best approach.

Lack of Real-Time Data:

One key factor contributing to inaccuracies in Zillow’s home valuations is the lack of real-time data. The real estate market is dynamic, influenced by ever-changing economic conditions, local developments, and other factors. Zillow’s algorithms might not always capture these changes promptly, leading to outdated valuations that don’t reflect the current market reality.

Limited Property-Specific Information:

Zillow relies on a range of data points to estimate home values, including recent sales in the area, tax assessments, and other public records. However, the platform may lack specific details about individual properties, such as recent renovations or unique features. Without access to this nuanced information, Zillow’s algorithm may struggle to provide accurate valuations for homes with distinctive characteristics.

Neighborhood Averages and Generalizations:

Zillow’s algorithms often rely on averages and generalizations for a given neighborhood, which can lead to inaccuracies for homes that deviate significantly from the local norm. Unique properties or those with specific features may not fit neatly into the algorithm’s calculations, resulting in valuations that don’t align with the property’s true value.

Market Volatility and Economic Factors:

Real estate markets can be subject to fluctuations influenced by economic conditions, interest rates, and other external factors. Zillow’s algorithms may not always account for these macroeconomic influences, leading to valuations that are not aligned with the broader market trends.

Limited Comparative Analysis:

While Zillow’s algorithm considers recent sales in the area, it may not always conduct a thorough comparative analysis of similar properties. Differences in the size, condition, or specific amenities of homes can significantly impact their market value, and Zillow’s valuation may fall short in providing an accurate reflection of these nuances.

While Zillow’s Home Value Zestimate can be a helpful starting point for estimating property values, it’s crucial for homeowners and prospective buyers to approach these valuations with a degree of caution. Real estate is a complex and nuanced field, and automated algorithms may not capture all the intricacies that influence a property’s value. Consulting with local real estate professionals, conducting thorough research, and considering a variety of factors beyond Zillow’s estimates will contribute to a more accurate understanding of a property’s true market value.

In Florida, wind mitigation inspections and four-point inspections are often required by insurance companies to assess the risk associated with insuring a home. However, there isn’t a specific age requirement for a home to undergo these inspections. Instead, the need for these inspections is often driven by the insurance company’s policies and the age and condition of the home.

Wind mitigation inspections focus on the home’s ability to withstand wind damage, and they may be required for homes of various ages, especially in areas prone to hurricanes and strong winds.

A four-point inspection typically examines four key areas: the roof, electrical system, plumbing system, and HVAC (heating, ventilation, and air conditioning) system. Insurance companies may request this inspection for older homes to assess the condition of these critical components.

To determine whether your home needs a wind mitigation or four-point inspection, it’s best to check with your insurance provider. They can provide specific information on their requirements and any applicable regulations in your area. Keep in mind that insurance requirements can vary, so it’s essential to communicate directly with your insurance company for accurate and up-to-date information.

When it comes to purchasing a home in Florida, potential buyers often encounter a unique aspect of the real estate landscape – Homeowners Associations (HOAs). HOAs play a significant role in many Florida communities, influencing the overall living experience for residents. In this blog post, we’ll explore what HOAs are, their functions, and key considerations for homebuyers thinking about joining an HOA-managed community in the Sunshine State. Navigating Homeowners Associations in Florida: A Guide for Prospective Homebuyers:

Understanding Homeowners Associations (HOAs): A Homeowners Association is a private governing body typically established by the developer or builder of a community. Its primary purpose is to manage and maintain common areas, enforce community rules, and enhance property values. Joining an HOA is often mandatory for residents within the community, and it involves paying regular fees to cover communal services and amenities.

Benefits of HOAs:

Aesthetically Pleasing Communities: HOAs enforce guidelines to maintain a cohesive and aesthetically pleasing neighborhood. This often includes landscaping standards, exterior home maintenance requirements, and architectural guidelines.

Shared Amenities: Many HOA communities offer shared amenities such as pools, parks, and recreational facilities. These features contribute to an enhanced living experience and can increase property values.

Community Harmony: HOAs establish rules and regulations to promote a harmonious living environment. These rules can address issues like noise control, pet regulations, and the appearance of properties.

Considerations for Prospective Homebuyers:

HOA Fees and Budgets: Before committing to a home within an HOA community, understand the monthly or annual fees and how they contribute to the association’s budget. This information will give you insight into the financial health of the HOA.

Covenants and Restrictions: Review the community’s covenants, conditions, and restrictions (CC&R). These documents outline the rules and regulations homeowners must adhere to. Make sure you are comfortable with the restrictions imposed by the HOA.

Reserve Funds: Inquire about the HOA’s reserve fund. A well-managed association will have a reserve fund set aside for major repairs or unexpected expenses. This helps prevent special assessments on homeowners.

Community Involvement: Attend HOA meetings or community events to get a sense of the community’s dynamics and the level of resident involvement. Understanding the community’s culture is crucial for a positive living experience.

Homeowners Associations in Florida play a crucial role in shaping the lifestyle and aesthetics of residential communities. As a prospective homebuyer, carefully assess the benefits, restrictions, and financial aspects of joining an HOA-managed community. By doing so, you’ll be better equipped to make an informed decision that aligns with your preferences and lifestyle.

Even with so much data showing home prices are actually rising in most of the country, there are still a lot of people who worry there will be another price crash in the immediate future. In fact, a recent survey from Fannie Mae shows that 23% of consumers think prices will fall over the next 12 months. That’s nearly one in four people who are dealing with that fear – maybe you’re one of them. Experts Project Home Prices Will Rise over the Next 5 Years.

To help ease that concern, here’s what the experts say will happen with home prices not just next year, but over the next five years.

Experts Project Ongoing Appreciation

While seeing a small handful of expert opinions may not be enough to change your mind, hopefully, a larger group of experts will reassure you. Here’s that larger group.

The Home Price Expectation Survey (HPES) from Pulsenomics is a great resource to show what experts forecast for home prices over a five-year period. It includes projections from over 100 economists, investment strategists, and housing market analysts. And the results from the latest quarterly release show home prices are expected to go up every year through 2027 (see graph below):

And while the projected increase in 2024 isn’t as large as 2023, remember home price appreciation is cumulative. In other words, if these experts are correct after your home’s value rises by 3.32% this year, it should go up by another 2.17% next year.

If you’re worried home prices are going to fall, here’s the big takeaway. Even though prices vary by local area, experts project they’ll continue to rise across the country for years to come at a pace that’s more normal for the market.

What Does This Mean for You?

If you’re not convinced yet, maybe these numbers will get your attention. They show how a typical home’s value could change over the next few years using the expert projections from the HPES. Check out the graph below:

In this example, let’s say you bought a $400,000 home at the beginning of this year. If you factor in the forecast from the HPES, you could potentially accumulate more than $71,000 in household wealth over the next five years.

The emerald waters, sugar-white sands, and vibrant coastal culture make Destin, Florida, a coveted destination for both vacationers and those seeking a permanent slice of paradise. As the sun sets on 2023, let’s take a closer look at the current state of the real estate market in this Gulf Coast gem. Navigating the Waves: A Deep Dive into the Current Real Estate Market in Destin, Florida.

Market Overview:

Destin’s real estate market has been experiencing dynamic shifts, influenced by various factors such as economic trends, demographic changes, and the impact of recent global events. As of now, the market remains robust, with a mix of opportunities for both buyers and sellers.

1. **Home Values and Appreciation:**

Home values in Destin have shown steady appreciation over the past few years. The combination of limited inventory and strong demand has contributed to a seller’s market, with property values experiencing healthy growth.

2. **Market Trends:**

The market is witnessing trends that cater to diverse preferences. Waterfront properties continue to be highly sought after, offering not only breathtaking views but also investment potential. Additionally, there is a growing interest in eco-friendly and sustainable homes, aligning with the community’s commitment to preserving its natural beauty.

3. **Tourism Impact:**

Destin’s thriving tourism industry significantly influences the real estate market. The popularity of short-term rentals has led to increased demand for vacation homes and investment properties. However, local regulations and community concerns are shaping how short-term rentals are managed.

4. **New Developments:**

The Destin skyline is evolving with several new developments. From luxury condominiums to master-planned communities, developers are capitalizing on the demand for modern amenities and lifestyle options. These developments often integrate retail, dining, and recreational spaces to create a holistic living experience.

Challenges and Considerations:

1. **Inventory Challenges:**

The limited inventory remains a challenge for both buyers and real estate professionals. While this scarcity may drive up property values, it can also make it more challenging for potential buyers to find their dream home.

2. **Regulatory Landscape:**

Local regulations, especially concerning short-term rentals, are a critical consideration for investors. Staying informed about zoning laws, rental restrictions, and community guidelines is essential for those looking to capitalize on the vacation rental market.

3. **Climate and Environmental Concerns:**

As climate change becomes a more pressing issue, prospective buyers are increasingly considering environmental factors. This includes potential risks such as hurricanes and rising sea levels, which can impact property values and insurance costs.

Conclusion:

Destin’s real estate market continues to ride the waves of change, offering both challenges and opportunities for investors, homeowners, and those seeking a piece of the coastal lifestyle. As the market adapts to emerging trends and challenges, staying informed and working with knowledgeable local real estate professionals remains key to navigating the currents of this dynamic market. Whether you’re looking for a vacation retreat, an investment property, or a permanent residence, Destin’s real estate market invites you to set sail on a journey of possibilities.

Survey: Sellers who go-it alone are twice as likely to be unsatisfied with the experience – and more likely to say their earlier opinion, “agents are overpaid,” was wrong. FSBO Sellers Regret Not Having an Agent.

Homeowners who decline to use a real estate agent to sell their property are twice as likely to say they weren’t satisfied with the selling experience, according to a new survey from Clever Real Estate of 1,000 home sellers in 2022 and 2023. Survey respondents say they realize they likely made less money on their home sale and faced more stress by not having a professional representative.

Those who didn’t use a real estate agent said before their transaction that they think pros are overpaid for what they do and are not more knowledgeable about the home selling process than the average seller. However, when these respondents reflected on their experience after the transaction, they admitted that they made some mistakes without the help of a pro.

More than a third of non-agent sellers, such as FSBOs (for sale by owner) or those selling to an iBuyer, said the process was more difficult than they expected. What’s more, these sellers admitted:

• Buyers distrusted them because they didn’t have an agent (43%)

• They struggled to understand their contract (40%)

• They made legal mistakes because they didn’t use an agent (36%)

The survey also found other consequences of going it alone as a seller:

• Lower sales price: Homeowners who sold without a real estate agent are three times more likely to say they lost money on their home sale. The Clever Real Estate survey found that those who sold their home with an agent tended to earn $46,603 more in average profits than those who sold without an agent in 2022 and 2023. About half of unrepresented sellers say they wish they had priced their home differently, and nearly half now believe their home would have sold for more if they would have used an agent.

• Longer selling process: Home sellers without an agent are nearly twice as likely to say they didn’t accept an offer for at least three months; 53% of sellers who used an agent say they accepted an offer within a month of listing their home. Yet many homeowners who didn’t use an agent said the primary reason for going it alone was to sell faster.

• More stress: Half of home sellers who did not use an agent admit to crying at some point in the process, and 52% of unrepresented home sellers said they felt overwhelmed by the entire sales process. On the flip side, homeowners who hired an agent were more likely to say they felt good about their sale and expressed less stress.

Home sellers who used an agent also had some gripes about their experience, albeit much fewer. But those who were unhappy with their agent experience expressed feelings like their agent was only looking to make a sale and didn’t care about their interests, their agent “annoyed” them, or they thought the agent pressured them into decisions, the survey found.

That said, 77% of respondents who used an agent say they were satisfied, and 72% say they would use their agent again.

Even though the vast majority of home searches start online, most consumers still use real estate agents to buy or sell a home. Indeed, the National Association of Realtors®’ (NAR) 2023 Profile of Home Buyers and Sellers found that 89% of buyers and sellers in the last year used a real estate agent, up from the previous year.

Only 7% of homeowners sold as a FSBO over the last year – which matches the all-time low recorded in 2021, according to NAR data. FSBOs continue to not fare as well in the market as professionally represented homes: FSBOs sold at a median price of $310,000 in the last year, compared to $405,000 for listed homes, NAR’s data shows.

“Having a Realtor help you navigate the homebuying and selling process provides peace of mind, especially in a challenging market with high prices, elevated mortgage rates and limited inventory,” says NAR President Tracy Kasper.

Most (72%) real estate investors say the market is as good or better than it was last year, and 75% expect stability or improvements over the next six months.

Real estate investors believe that market conditions have improved and will continue to get better in the coming months according to the Fall 2023 Investor Sentiment Survey from RCN Capital, conducted by market intelligence firm CJ Patrick Company. Almost three quarters of the investors surveyed (72%) said market conditions for investing were better or the same as a year ago, and 75% believed conditions would improve or remain stable over the next six months.

“Despite higher home prices, higher financing costs, and limited inventory, real estate investors continue to express optimism about market opportunities today and in the months ahead,” said RCN Capital CEO Jeffrey Tesch. “Investors continue to play an important role in the housing market according to a recent report from CoreLogic, more than one in four home sales is to an investor, and we continue to see interest from both rental property buyers and fix-and-flip investors in our business.”

The Fall 2023 Investor Sentiment Survey is the second quarterly report from RCN Capital taking the pulse of real estate investors across the country, identifying market challenges and opportunities, and getting feedback on current trends and events.

Investor sentiment on the current state of the real estate market improved from the Spring 2023 Survey, with 49% saying conditions are better than they were a year ago compared to 30% in the spring. Views on the market six months from now also improved, with 44% believing conditions will improve, up from 30% in the prior survey.

Despite the optimism, investors are moving forward prudently: only 22% plan to buy more properties than they did a year ago; 39% plan to buy the same number; and 39% plan to buy fewer.

“Interestingly, fix-and-flip investors seem much more optimistic about future opportunities 50% of them believe that conditions will improve over the next six months compared to just 24% of rental property investors,” noted Rick Sharga, CJ Patrick Company CEO. “That may be an indication that flipping activity has bottomed out, but may also be a reflection of current challenges in the rental market, with rates continuing to decline even as more rental inventory comes online.”

Investors continued to see the impact of higher mortgage rates in their local markets. Over 30% have seen a decline in demand for owner-occupied homes; almost 21% have seen an increase in demand for rental properties; and 37% have noted both trends.

Recession seems likely, but home prices expected to rise

Despite being somewhat optimistic about the market environment going forward, over half of those surveyed (53%) believed that the U.S. would enter a recession in 2023 or 2024. Only 18% said that the country would avoid a recession, while 29% were unsure.

But even with a recession looming, investors overwhelmingly believe that home prices will continue to increase almost 53% expect home prices to go up, 22% believe prices will remain about the same, and 24% believe they’ll decrease.

Main challenges: High finance costs, limited inventory, competition

Obstacles cited by investors in the fall survey mirrored those mentioned most often in the spring survey, and remain the main concerns by investors in the months ahead.

The high cost of financing was the biggest issue among investors, being mentioned almost 76% of the time, while lack of inventory was mentioned over 42%. Competition from other buyers clearly remains an issue in today’s low inventory environment, with competition from institutional investors noted by 33% of the respondents and competition from consumer homebuyers by 29%.

Other challenges mentioned frequently included difficulty in securing a loan (22%) and supply chain delays (22%).

Most investors stay close to home

A new question added to the fall survey asked investors where they purchased their investment properties. Most focus close to home: 44% purchase within their hometown, and 79% within their home state. There were no significant differences in purchase distances between fix-and-flip and rental property investors.

While there’s been a lot of concern prices would come crashing down this year, data shows that didn’t happen. In fact, home prices are rising in most of the nation. Experts say that trend will continue, just at a slower pace that’s much more normal for the housing market – and that’s a good thing.

To help show just how confident experts are in this continued appreciation, take a look at the Home Price Expectation Survey from Pulsenomics. It’s a survey of a national panel of over 100 economists, real estate experts, and investment and market strategists. As the graph below shows, the consensus is, that prices will keep climbing next year, and in the years to come.

The site-built home process hasn’t changed much over the decades, but modular building makes it more efficient by completing different tasks at the same time. Modular Housing CEO: Solution to Chronic Shortage

Most traditional homebuilders in America follow a construction process that’s hardly changed in decades, and which typically takes about four to six months, if not longer, to deliver a completed single-family home.

Modular homebuilders fabricate walls, roofing and other segments of a home in a factory and then deliver the finished sections to the homesite for assembly in a process that takes just a few weeks to complete.

Veev, a modular homebuilder based in Hayward, California, has built more than 170 townhomes, single-family houses, condos and other types of dwellings around the Bay Area and has set its sights on building 300 more single-family houses in Northern California by the end of 2025.

CEO Amit Haller, who co-founded Veev in 2008, recently spoke to The Associated Press about how more modular home construction could help tackle the nation’s chronic shortage of new homes. The interview has been edited for length and clarity.

Question: What are some of the major differences in how Veev builds a home versus a traditional homebuilder?

Answer: The traditional way is a very sequential process. There’s the excavation. And then there’s the concrete. Then you need to wait for three weeks until the concrete will be fully load-bearing. And then there’s the framers. And after the framers there’s the electricians and the plumber, etc. So, it’s a very, very sequential process. Now, say that you take this entire process and squeeze it into one linear production line doing a wall. It becomes very similar to a production line of a car, but in this production when we are doing it wall by wall, and with our unique plug-and-play method, those walls are clicked one to another in the field, very quickly, very efficiently.

Question: How many workers does it take to build a Veev fabricated home?

Answer: It’s a mix of workers, who are uniquely certified on the build system. And obviously, we have machines and robots from time to time. Still, it’s not zero human touch. There’s stuff that a human is always going to do better than a robot and some stuff is going to be much safer to give to the robot. It’s always going to be a blended human and machine environment.

Question: Once you deliver all the components for assembly on site, how many workers do you need to finish the job?

Answer: It’s a team of five people that will assemble the home in four weeks, from foundation to finishing.

Question: So it’s fair to say you’re insulated from a lot of the labor shortage challenges many homebuilders have complained about for years?

Answer: It’s the labor shortage and the labor experience. Because the shortage is also generating the fact that there’s less and less experience within the labor.

It takes many years to become a good framer, or painter or roofer, or obviously, plumbers or electricians. So what we see actually is the fact that not only homes are becoming more expensive, the quality actually decreases. The home that you buy today from a builder is exactly the same home they did 50 years ago. Maybe better appliances, but that’s pretty much it.

Question: Your business model saves on labor and other costs, but you still face the same challenges and delays traditional builders do in finding ready to build land, correct?

Answer: The cost of a home is made with several elements, land is about 25% of it. But about 50% of the cost of the homes is literally the construction. So, no, we are not solving for the land, but what we are solving for is to tackle probably the most expensive component in this process and the time that it takes. So, it could take you like two years to entitle land, sometimes even three or four years, but then it might take you another year to build it. We can build it in a month.

Question: New home construction slowed sharply for many years after the late 2000s housing crash. Do you expect more builders like Lennar will adopt the prefabrication approach to more quickly build homes?

Answer: Absolutely, because the consistent erosion of the current industry is very visible and very clear in the past 10 years. Veev is not the only solution. And I think there’s going to be a handful, if not a dozen different options. And the good news is there’s room for everyone, including the traditional industry, because the shortage is so serious and so real that it’s not going to be a one-company fix.

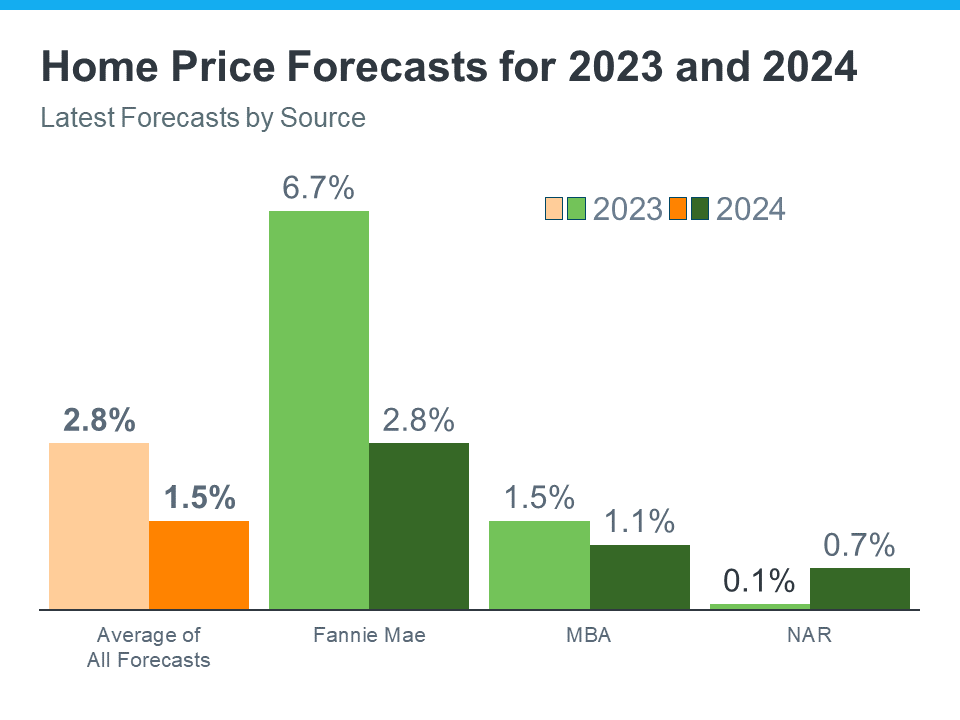

The new year is right around the corner, and you might be wondering if 2024 will be the right time to buy or sell a home. If you want to make the most informed decision possible, it’s important to know what the experts have to say about what’s ahead for the housing market. Spoiler alert: the projections may be better than you think. Here’s why.

As you can see in the orange bars on the left, on average, experts forecast prices will end this year up about 2.8% overall, and increase by another 1.5% by the end of 2024. That’s big news, considering so many people thought prices would crash this year. The truth is, prices didn’t come tumbling way down in 2023, and that’s because there just weren’t enough homes for sale compared to the number of people who wanted or needed to buy them, and that inventory crunch is still very real. This is the general rule of supply and demand, and it continues to put upward pressure on prices as we move into the new year.

Looking forward, experts project home prices will continue to rise next year, but not quite as much as they did this year. Even though the expected rise in 2024 isn’t as big as in 2023, it’s important to understand home price appreciation is cumulative. In simpler terms, this means if the experts are right, according to the national average, after your home’s value goes up by 2.8% this year, it should go up by another 1.5% next year. That ongoing price growth is a big part of why owning a home can be a smart decision in the long run.

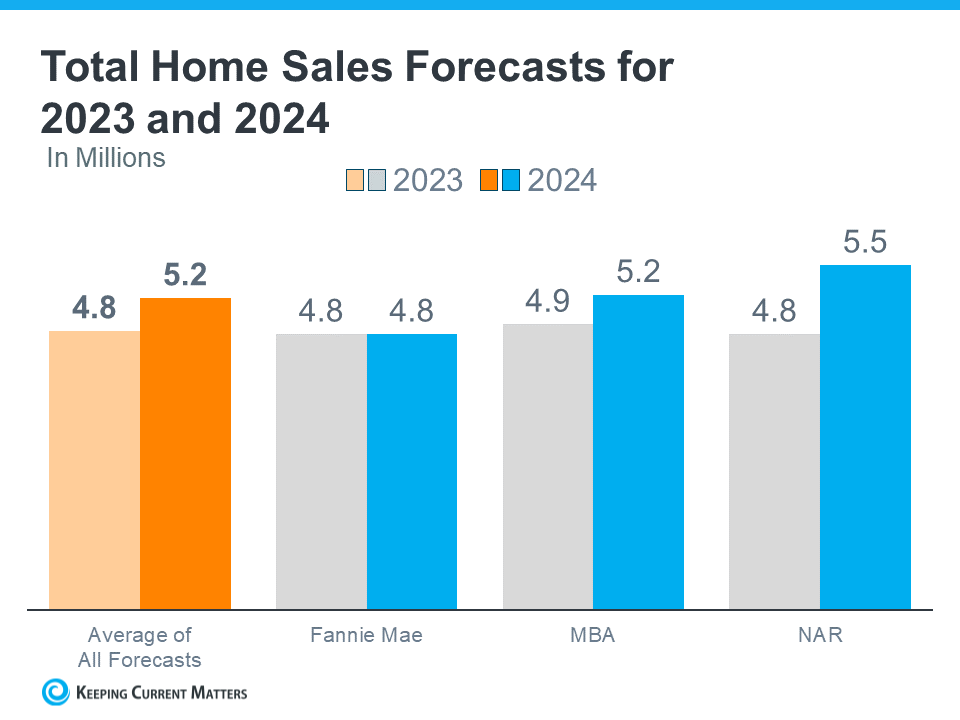

Projections Show Sales Should Increase Slightly Next Year

While 2023 hasn’t seen a lot of home sales relative to more normal years in the housing market, experts are forecasting a bit more activity next year. Here’s what those same three organizations project for the rest of this year, and in 2024 (see graph below):

While expectations are for just a slight uptick in total sales, improved activity next year is a good thing for the housing market, and for buyers and sellers like you. As people continue to move, that opens up options for hopeful buyers who are looking for a home.

So, what do these forecasts show? The housing market is expected to be more active in 2024. That may be in part because there will always be people who need to move. People will get new jobs, have children, get married or divorced – these and other major life changes lead people to move regardless of housing market conditions. That will remain true next year, and for years to come. And if mortgage rates come down, we’ll see even more activity in the housing market.

Bottom Line

If you’re thinking about buying or selling, it’s important to know what the experts are forecasting for the future of the housing market. When you’re in the know about what’s ahead, you can make the most informed decision possible. Connect with a local real estate agent to chat about the latest forecasts, and craft a plan for your next move.

Since today’s buyers are already dealing with higher rates and prices, you’ll want to assist them with another cost: a property’s homeowners association or HOA.

Membership in an HOA is mandatory for residents, with fees paid to maintain shared areas such as pools and landscaping. Although HOAs are a common part of condo and townhome lifestyles, a growing number of single-family homeowners are paying HOA dues.

HOA fees vary widely and may increase with little notice. There are also a few stories of fanatical HOA boards using fines or even foreclosure threats to enforce unpopular rules.

While buyer’s agents aren’t required to discuss a property’s HOA, it’s smart to offer guidance if needed. Here are some tips to share:

Ask for copies of all HOA covenants, bylaws, rules and regulations, and meeting minutes.

Research the HOA’s budget and reserve funds, and how often it has raised members’ fees.

Search the county website for HOA-filed liens, judgments or foreclosures.

Look at the HOA’s attorney fees. Excessive amounts suggest that the board is having legal issues, creating rules opposed by members, or both.

Attend an HOA meeting, if possible, to watch interactions between management and members.

In the face of high interest rates and rising home prices, the typical buyer’s income rose 22% to $107K. 1 out of 3 (32%) was a first-time buyer, and 89% used an RE agent.

What does the typical buyer look like in 2023? The typical seller?

The National Association of Realtors® (NAR) released its 2023 Profile of Home Buyers and Sellers this week. The annual survey tracked transactions between July 2022 and June 2023. It was first published in 1981 to give industry professionals a detailed insight into current home buying and selling behavior.

Median household income for 2023 homebuyers skyrocketed year-to-year, rising to $107,000 from $88,000 only one year earlier.

“Given the erosion of housing affordability due to higher home prices and mortgage rates, the household income for those who successfully purchased homes jumped by nearly $20,000 and topped six figures for only the second time in our records,” says Jessica Lautz, NAR deputy chief economist and vice president of research. “In a still-competitive housing market, more well-off homebuyers were able to have their bids accepted by offering larger down payments and even by paying cash.”

First-time buyers made inroads in the 2023 study. Those new to the market made up about one in three sales (32%) – up from 2022’s one in four ( 26%). However, that percentage is still notably lower than the 38% annual average in earlier years, starting in 1981.

The typical ages for first-time (35 years) and repeat (58 years) buyers declined slightly from the record highs of 36 years and 59 years, respectively, last year.

“First-time buyers tiptoed back into the market this year with less competition and fewer multiple-offer scenarios,” says Lautz. “While the share of first-time buyers is still near historic lows, it is higher than last year.”

Household composition also continues to shift: 70% of recent buyers did not have a child under the age of 18 in their home, the highest share recorded. By comparison, in 1985, just 42% of households did not have a child under the age of 18.

Three out of five (49%) of recent buyer couples were married couples – the lowest share since 2010 – while 9% were unmarried. More buyers were also going it alone: Single-female buyers (19%) and single male buyers (10%) both increased.

Based on type of property, 14% purchased a multi-generational home. The top reasons for doing so were to take care of aging parents, save money and accommodate children or relatives over the age of 18 who were moving back home.

Racial diversity: In terms of homebuyers’ race:

81% were white/Caucasian

7% were Hispanic/Latino

7% were Black/African American

6% were Asian/Pacific Islander

6% identified as some other race

One in 10 (10%) of buyers were born outside the U.S., up from 8% last year, and 6% spoke a primary language other than English, up from 5% last year.

“Homebuyers in the past year were more diverse, both racially and ethnically, with increases noted among minority buyers, buyers who were born outside of the U.S. and buyers whose primary language is not English,” says Lautz. “This shows encouraging signs that the homeownership rate may narrow in the future as more minority buyers enter the market.”

Distance from home: The median distance between the home recent buyers purchased and the home from which they moved was 20 miles, a decline from 50 miles 2022 and closer to the previous norm of 15 miles.

Similarly, while suburbs boomeranged back (47% in the 2023 report, up from 39% in the 2022 report), they remain under the levels seen in 2017 to 2021 when they made up more than half of all buyers. At the same time, small towns and rural areas remain more popular than they were over the same period.

Home financing: 80% of buyers financed their home purchase, up slightly from 78% last year but down from 87% two years ago.

The typical down payment for first-time buyers was 8% – the highest since 1997 when it was 9%. The typical down payment for repeat buyers was 19%, the highest since 2005 when it was 21%.

In securing down payments, first-time buyers increased their reliance on financial assets this year, using the sale of stocks or bonds (11%), 401k or pensions (9%), IRAs (2%) and/or the sale of cryptocurrency (2%).

Realtor services: Nine out of 10 buyers (89%) relied on the services of a real estate agent or broker – an increase from 86% last year. Of those, 90% would use their agent again or recommend their agent to others.

On the selling side, 89% of home sellers worked with a real estate agent to sell their home – an increase from 86% the year before.

“While the housing market had limited inventory and home prices were in flux, buyers and sellers both increased their use of real estate agents,” says Lautz. “Buyers wanted an expert to help them find the right home and conduct negotiations. Sellers relied on real estate agents and brokers to price their home competitively and market it to potential buyers.”

The typical home seller was 60 years old – unchanged from last year’s report. Sellers typically lived in their homes for 10 years before selling.

“Having a Realtor® help you navigate the home buying and selling process provides peace of mind, especially in a challenging market with high prices, elevated mortgage rates and limited inventory,” says NAR President Tracy Kasper. “Buyers and sellers can rely on Realtors’ expertise to shepherd them through one of life’s biggest and most important purchases.”

There is a lot of talk in the news about real estate agent commissions. They LOVE what they do and they do it because they LOVE helping people but there is almost always a huge misconception on what they do and how they get paid. It’s not a secret so here ya go…😊

The average FULL TIME REALTOR’s earnings last year was $31,900 @ 40+ hours a week. (Notice I wrote full time 40+ hours not 0-20 hours a week) which is well below the living wage. As a REALTOR they do not get paid a hourly wage or salary and they

only get paid if they sell a home and it closes. They can only get paid by broker to broker. As an agent you could work with someone days, weeks, months, or years with no guarantee of a sale ever.

Essentially they wake up each day unemployed going on Job Interviews and they deal with constant rejection. They dedicate time away from family, use our time, gas, pay for babysitters, miss dinner and weekends and rarely take vacations. They are on 24/7! You constantly need to be on, or you could miss an opportunity. Once they do close a home, half goes to the other persons agent from the remaining half. They have lots of upfront expenses that must be paid out before they even get paid:

Broker Splits and Fees

Office rent and utilities

MLS Fees

NAR Fees

Local Association Fees

E&O Business Insurance

Extended Auto Insurance

Self-Employment Tax

State Licensing Fees

Advertising Fees

Showing Service Fees

Website Fees

Assistant’s Salaries

Showing partners

Transaction coordinator

Yard Signs

Photographers

Videographers

Office Supplies

Business Cards

Property Flyers

Electronic Lockboxes

Continued RE Education

Legal Fees

Gas

Income taxes are not taken out so they have to put that aside around 25-30%.

Don’t forget health insurance if you don’t have a spouse who provides it.

As a listing agent they have lots of tasks far more than just selling a home.

1. Prepare Listing Presentation for Sellers

2. Research Sellers Property Tax Info

3. Research Comparable Sold Properties for Sellers

4. Determine Average Days on Market

5. Gather Info From Sellers About Their Home

6. Meet With Sellers at Their Home

7. Get To Know Their Home

8. Present Listing Presentation

9. Advise on Repairs and/or Upgrades

10. Provide Home Seller To-Do Checklist

11. Explain Current Market Conditions

12. Discuss Seller’s Goals

13. Share Your Value Proposition

14. Explain Benefits of Your Brokerage

15. Present Your Marketing Options

16. Explain Video Marketing Strategies

17. Demonstrate 3D Tour Marketing

18. Explain Buyer & Seller Agency Relationships

19. Describe the Buyer Pre-Screening Process

20. Create Internal File for Transaction

21. Get Listing Agreement & Disclosures Signed

22. Provide Sellers Disclosure Form to Sellers

23. Verify Interior Room Sizes

24. Obtain Current Mortgage Loan Info

25. Confirm Lot Size from County Tax Records

26. Investigate Any Unrecorded Property Easements

27. Establish Showing Instructions for Buyers

28. Agree on Showing Times with Sellers

29. Discuss Different Types of Buyer Financing

30. Explain Appraisal Process and Pitfalls

31. Verify Home Owners Association Fees

32. Obtain a Copy of HOA Bylaws

33. Gather Transferable Warranties

34. Determine Need for Lead-Based Paint Disclosure

35. Verify Security System Ownership

36. Discuss Video Recording Devices & Showings

37. Determine Property Inclusions & Exclusions

38. Agree on Repairs to Made Before Listing

39. Schedule Staging Consultation

40. Schedule House Cleaners

41. Install Electronic Lockbox & Yard Sign

42. Set-Up Photo/Video Shoot

43. Meet Photographer at Property

44. Prepare Home For Photographer

45. Schedule Drone & 3D Tour Shoot

46. Get Seller’s Approval of All Marketing Materials

47. Input Property Listing Into The MLS

48. Create Virtual Tour Page

49. Verify Listing Data on 3rd Party Websites

50. Have Listing Proofread

51. Create Property Flyer

52. Have Extra Keys Made for Lockbox

53. Set-Up Showing Services

54. Help Owners Coordinate Showings

55. Gather Feedback After Each Showing

56. Keep track of Showing Activity

57. Update MLS Listing as Needed

58. Schedule Weekly Update Calls with Seller

59. Prepare “Net Sheet” For All Offers

60. Present All Offers to Seller

61. Obtain Pre-Approval Letter from Buyer’s Agent

62. Examine & Verify Buyer’s Qualifications

63. Examine & Verify Buyer’s Lender

64. Negotiate All Offers

65. Once Under Contract, Send to Title Company

66. Check Buyer’s Agent Has Received Copies

67. Change Property Status in MLS

68. Deliver Copies of Contact/Addendum to Seller

69. Keep Track of Copies for Office File

70. Coordinate Inspections with Sellers

71. Explain Buyer’s Inspection Objections to Sellers

72. Determine Seller’s Inspection Resolution

73. Get All Repair Agreements in Writing

74. Refer Trustworthy Contractors to Sellers

75. Meet Appraiser at the Property

76. Negotiate Any Unsatisfactory Appraisals

77. Confirm Clear-to-Close

78. Coordinate Closing Times & Location

79. Verify Title Company Has All Docs

80. Remind Sellers to Transfer Utilities

81. Make Sure All Parties Are Notified of Closing Time

82. Resolve Any Title Issues Before Closing

83. Receive and Carefully Review Closing Docs

84. Review Closing Figures With Seller

85. Confirm Repairs Have Been Made

86. Resolve Any Last Minute Issues

87. Attend Seller’s Closing

88. Pick Up Sign & Lock Box

89. Change Status in MLS to “Sold.”

90. Close Out Seller’s File With Brokerage

As a buyers agent they also have many tasks.

1. Schedule Time To Meet Buyers

2. Prepare Buyers Guide & Presentation

3. Meet Buyers and Discuss Their Goals

4. Explain Buyer & Seller Agency Relationships

5. Discuss Different Types of Financing Options

6. Help Buyers Find a Mortgage Lender

7. Obtain Pre-Approval Letter from Their Lender

8. Explain What You Do For Buyers As A Realtor

9. Provide Overview of Current Market Conditions

10. Explain Your Company’s Value to Buyers

11. Discuss Earnest Money Deposits

12. Explain Home Inspection Process

13. Educate Buyers About Local Neighborhoods

14. Discuss Foreclosures & Short Sales

15. Gather Needs & Wants Of Their Next Home

16. Explain School Districts Effect on Home Values

17. Explain Recording Devices During Showings

18. Learn All Buyer Goals & Make A Plan

19. Create Internal File for Buyers Records

20. Send Buyers Homes Within Their Criteria

21. Start Showing Buyers Home That They Request

22. Schedule & Organize All Showings

23. Gather Showing Instructions for Each Listing

24. Send Showing Schedule to Buyers

25. Show Up Early and Prepare First Showing

26. Look For Possible Repair Issues While Showing

27. Gather Buyer Feedback After Each Showing

28. Update Buyers When New Homes Hit the Market

29. Share Knowledge & Insight About Homes

30. Guide Buyers Through Their Emotional Journey

31. Listen & Learn From Buyers At Each Showing

32. Keep Records of All Showings

33. Update Listing Agents with Buyer’s Feedback

34. Discuss Home Owner’s Associations

35. Estimate Expected Utility Usage Costs

36. Confirm Water Source and Status

37. Discuss Transferable Warranties

38. Explain Property Appraisal Process

39. Discuss Multiple Offer Situations

40. Create Practice Offer To Help Buyers Prepare

41. Provide Updated Housing Market Data to Buyers

42. Inform Buyers of Their Showing Activity Weekly

43. Update Buyers On Any Price Drops

44. Discuss MLS Data With Buyers At Showings

45. Find the Right Home for Buyers

46. Determine Property Inclusions & Exclusions

47. Prepare Sales Contract When Buyers are Ready

48. Educate Buyer’s On Sales Contract Options

49. Determine Need for Lead-Based Paint Disclosure

50. Explain Home Warranty Options

51. Update Buyer’s Pre-Approval Letter

52. Discuss Loan Objection Deadlines

53. Choose a Closing Date

54. Verify Listing Data Is Correct

55. Review Comps With Buyers To Determine Value

56. Prepare & Submit Buyer’s Offer to Listing Agent

57. Negotiate Buyers Offer With Listing Agent

58. Execute A Sales Contract & Disclosures

59. Once Under Contract, Send to Title Company

60. Coordinate Earnest Money Drop Off

61. Deliver Copies to Mortgage Lender

62. Obtain Copy of Sellers Disclosure for Buyers

63. Deliver Copies of Contract/Addendum to Buyers

64. Obtain A Copy of HOA Bylaws

65. Keep Track of Copies for Office File

66. Coordinate Inspections with Buyers

67. Meet Inspector At The Property

68. Review Home Inspection with Buyers

69. Negotiate Inspection Objections

70. Get All Agreed Upon Repair Items in Writing

71. Verify any Existing Lease Agreements

72. Check In With Lender To Verify Loan Status

73. Check on the Appraisal Date

74. Negotiate Any Unsatisfactory Appraisals

75. Coordinate Closing Times & Location

76. Make Sure All Documents Are Fully Signed

77. Verify Title Company Has Everything Needed

78. Remind Buyers to Schedule Utilities

79. Make Sure All Parties Are Notified of Closing Time

80. Solve Any Title Problems Before Closing

81. Receive and Review Closing Documents

82. Review Closing Figures With Buyers

83. Confirm Repairs Have Been Made By Sellers

84. Perform Final Walk-Through with Buyers

85. Resolve Any Last Minute Issues

86. Get CDA Signed By Brokerage

87. Attend Closing with Buyers

88. Provide Home Warranty Paperwork

89. Give Keys and Accessories to Buyers

90. Close Out Buyer’s File Brokerage

Whew…exhausting isn’t it!?! 🤯

✨You don’t need to buy or sell a home to support your agents real estate business – here are just a few simple ways to show your support! By sharing one of their listings, sending a friend or family member their way, letting them connect you with agents outside their area for a broker to broker referral, or leaving them a positive comment or review, this helps them feel seen and supported – (thanks to you)! ❤️✨

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

What does the typical buyer look like in 2023? The typical seller?

What does the typical buyer look like in 2023? The typical seller?