Let’s be real – buying a home right now is tough. You’re scrolling through listings, rushing to open houses, and maybe even losing out to more competitive offers. Somewhere along the way, you might’ve heard the reason it’s so hard to find a home is because big Wall Street investors are swooping in and snatching up everything in sight.

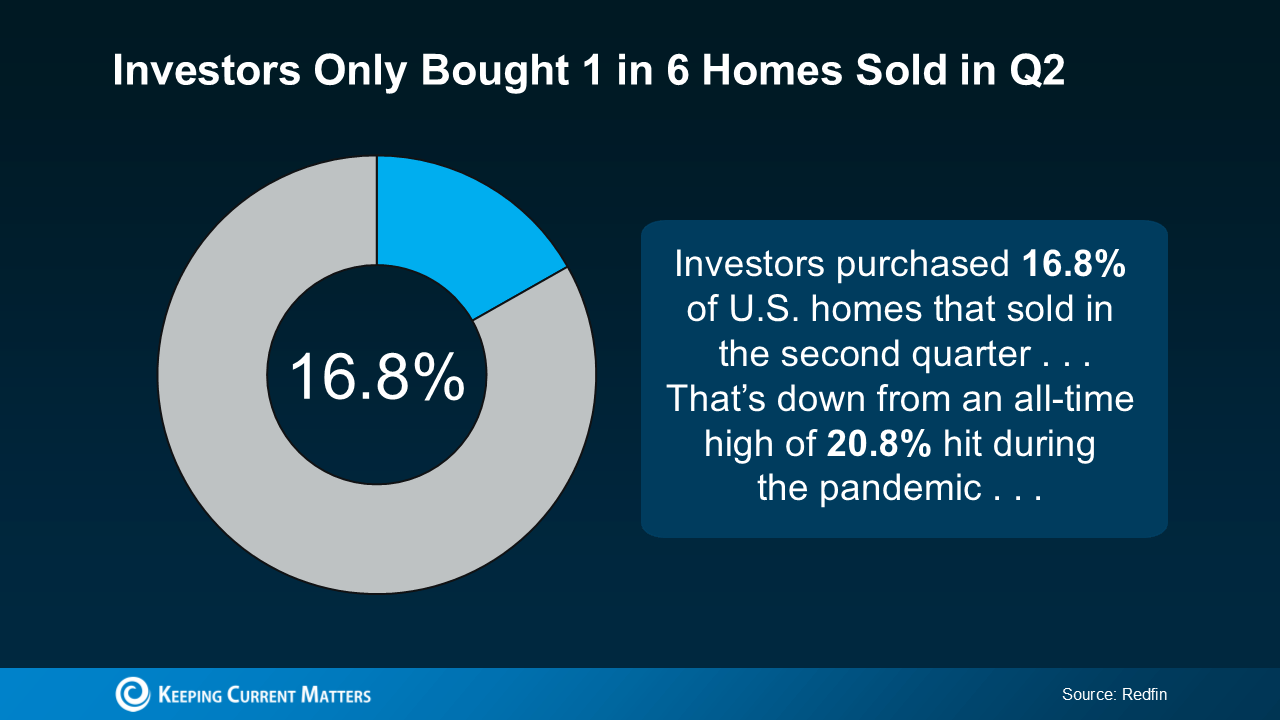

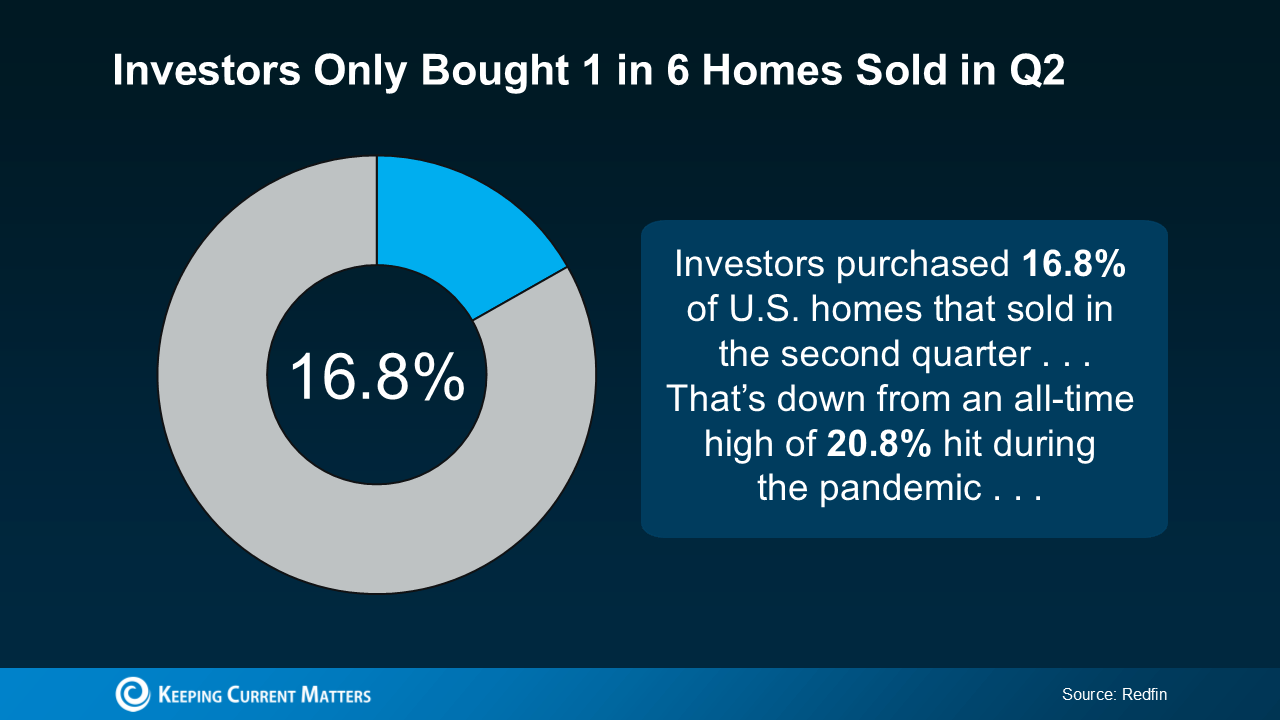

But here’s the thing: that’s mostly a myth. While investors are part of the market, according to Redfin, they’re a relatively small part:

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

So, before you get discouraged, let’s take a look at what’s really going on. You might be surprised to learn that Wall Street isn’t the competition you may think it is.

Most Investors Are Small Mom-and-Pops

Most investors aren’t the mega corporations you’ve probably heard about. In fact, many are your neighbors. A recent report from CoreLogic shows most investors are small, mom-and-pop types who own fewer than 10 properties. They aren’t massive companies with endless resources. Picture your neighbor who has another home they’re renting out or a vacation getaway.

Only about 1% of the market is owned by large, mega investors with thousands of properties. The majority are still owned by individuals and smaller investors – not the Wall Street giants.

Investor Purchases Are Declining

Not only are most investors small, but overall investor purchases have been on the decline. As the same report from CoreLogicsays:

“Investors made 80,000 purchases in June 2024, compared with 112,000 in June 2023, and a nearly 50% percent drop from the high of 149,000 purchases in June 2021 . . .”

And what does this mean going forward? CoreLogic goes on to point out this downward trend is expected to continue into 2025.

So, if it seems like competition with investors is pushing you out of the market, it might help to know that investor activity is actually slowing down.

Bottom Line

The idea that Wall Street is buying up all the homes is largely a myth. Most investors are small ones, and the share of homes purchased by investors is declining – so you can take this one off your worry list.

If you have questions about the housing market, talk to a local real estate agent. They can explain what’s really happening.

When you’re ready to move, figuring out what to do with your house is a big decision. And today, more homeowners are considering renting their home instead of selling it.

Recent data from Zillow shows about two-thirds (66%) of sellers thought about renting their home before listing, with nearly a third (28%) taking that possibility seriously. Compared to 2021, when fewer than half (47%) of homeowners considered renting before selling, it’s clear this trend is on the rise.

So, should you sell your house and use the money toward your next home or keep it as a rental to build long-term wealth? Let’s walk through some important questions to help you determine the right path for your financial and lifestyle goals.

Is Your House a Good Fit for Renting?

Before you decide what to do, it’s important to think about if it would make a good rental in the first place. For instance, if you’re moving far away, managing ongoing maintenance could become a major hassle. Other factors to consider are if your neighborhood is ideal for rentals and if your house needs significant repairs before it’s ready for tenants.

If any of these situations sound familiar, selling might be a more practical choice.

Are You Ready for the Realities of Being a Landlord?

Managing a rental property involves more than collecting monthly rent. It’s a commitment that can be time-consuming and challenging.

For example, you may get maintenance calls at all hours of the day or discover damage that needs to be repaired before a new tenant moves in. There’s also the risk of tenants missing payments or breaking their lease, which can add unexpected stress and financial strain. As Redfin notes:

“Landlords have to fix things like broken pipes, defunct HVAC systems, and structural damage, among other essential repairs. If you don’t have a few thousand dollars on hand to take care of these repairs, you could end up in a bind.”

Do You Understand the Costs?

If you’re considering renting primarily for passive income, remember, there are additional costs you should anticipate. As an article from Bankrate explains:

Mortgage and Property Taxes: You still need to pay these expenses, even if the rent doesn’t cover all of it.

Insurance: Landlord insurance typically costs about 25% more than regular home insurance, and it’s necessary to cover damages and injuries.

Maintenance and Repairs: Plan to spend at least 1% of the home’s value annually, more if the house is older.

Finding a Tenant: This involves advertising costs and potentially paying for background checks.

Vacancies: If the property sits empty between tenants, you’ll lose rental income and have to cover the cost of the mortgage until you find a new tenant.

Management and HOA Fees: A property manager can ease the burden, but typically charges about 10% of the rent. HOA fees are an additional cost too, if applicable.

Bottom Line

To sum it all up, selling or renting out your home is a personal decision. Make sure to weigh the pros and cons carefully and consult with professionals so you feel supported and informed as you make your decision. A real estate agent can be a great person to go to for advice.

As you’re getting ready to sell your house, one of the first questions you’re probably asking is, “how long is this going to take?” And that makes sense—you want to know what to expect.

While every market is different, understanding what’s happening nationally can give you a good baseline. But for an even more detailed look at real estate conditions in your area, connect with a local real estate agent. They know your local market best and can explain what’s happening near you and how it compares to national trends.

Here’s a look at some of the things a great agent will walk you through during that conversation.

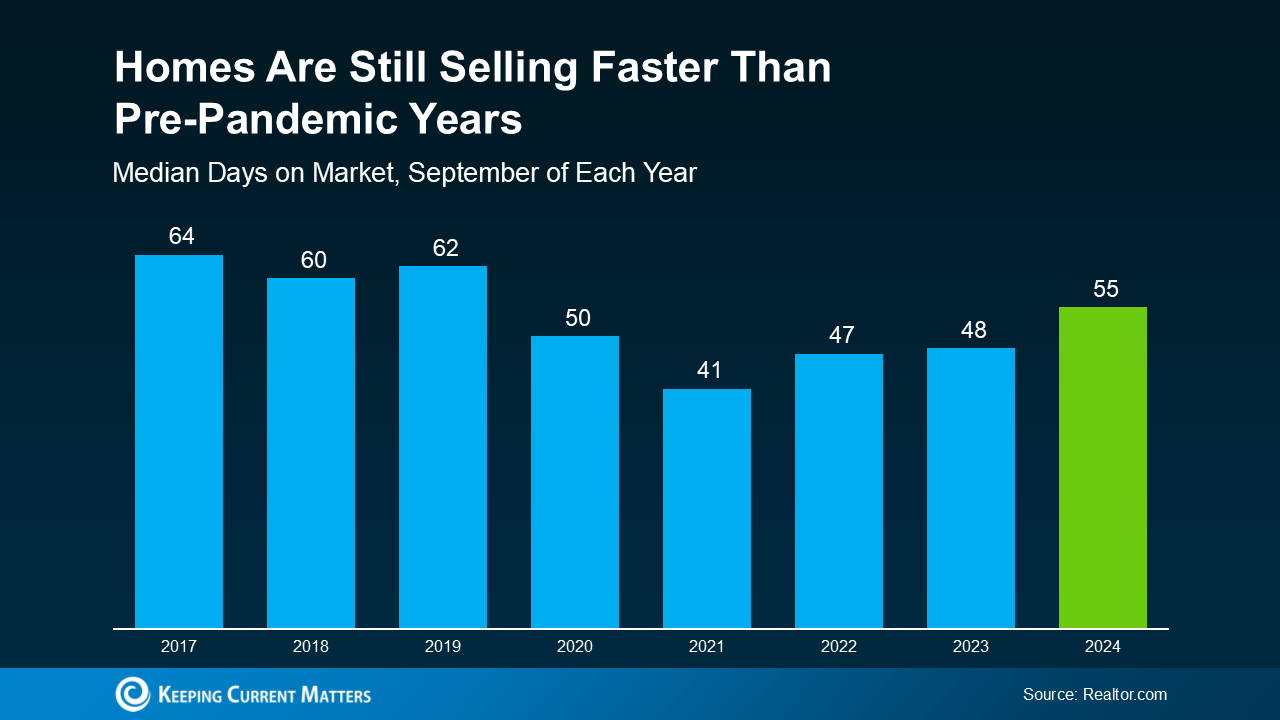

More Homes Are on the Market, and That’s Affecting How Long They Take To Sell

According to Realtor.com, the number of homes for sale has been going up this year. That means there are more options for buyers, which is great news for anyone looking to buy a home. But as a seller, it also means homes are staying on the market a bit longer now that buyers have more options to choose from (see graph below):

One of the big reasons homes sold so fast in recent years is because there were so few of them for sale. And now that there are more houses on the market, it makes sense that they aren’t selling at quite the same pace. Right now, according to Realtor.com, it takes 55 days from the time a house is listed for it to be officially sold and closed on.

But keep this in mind. While homes might not be selling as quickly as they did last year at this time, they’re still selling faster than they did in more normal years in the housing market, before the pandemic.

If you look back at 2017-2019 in the graph above, you’ll see that it was typical for a house to take 60 days or more to sell. So, today’s process is still faster than the norm.

That’s because, even with more homes for sale, there are still more buyers than homes for sale. So, homes that show well and are priced right are selling fast. As NerdWallet explains:

“Overall, though, demand still outpaces supply. This is hardly a mellow market: Good homes sellquickly . . .”

Your Agent Can Help Your Home Stand Out

If you’re looking for ways to make your move happen as quickly as possible, partnering with a great local agent is the key. Your real estate agent will help you with everything from setting the right price to staging your home so it looks its best. They’ll even create a marketing plan that grabs buyers’ attention and will give you key insights about what’s happening in your specific area, so you can plan accordingly and make the process go as smoothly as possible.

So, while homes might be on the market a little longer than before, they’re still selling faster than the norm. If you have the right agent and the right strategy in place, your house may even sell faster than you’d expect.

Bottom Line

If you’re planning to sell your house, knowing how long it might take is a big part of planning your next steps. By working with a local expert, you’ll be able to price, market, and sell your home with confidence.

Why a Destin Florida Vacation Home Is the Ultimate Summer Upgrade

Summer is officially here and that means it’s the perfect time to start planning where you want to vacation and unwind this season. If you’re excited about getting away and having some fun in the sun, it might make sense to consider if owning your own vacation home is right for you.

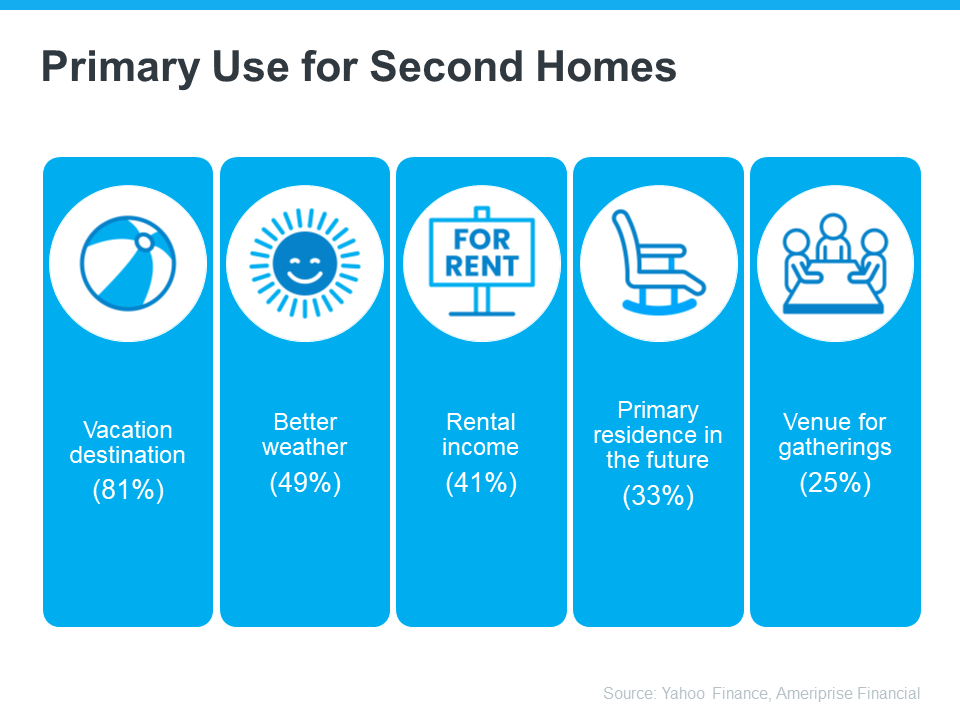

An Ameriprise Financial survey sheds light on why people buy a second, or vacation, home (see below):

Vacation destination or a place to get away from the stresses of everyday life (81%) – Having a second home to use as a vacation spot can be a special place where you go to relax and take a break from your daily routines and stressors. It also means you won’t have to worry about finding somewhere to stay when you go there.

Better weather (49%) – Buying in a place where there may be nicer weather can be a great escape, especially if it’s cold or rainy where you usually live. It lets you enjoy sunny days and warm temperatures, even when it’s not so nice back home.

Rental income (41%) – You can rent it out to other people when you’re not using it, which can help you make some extra money.

Primary residence in the future (33%) – You can eventually move into the home full-time during retirement. That means you can enjoy vacations there now and have a getaway ready for your future.

Having a venue for gatherings with family and friends (25%) – It would be a special spot where you can have parties, regular family trips, and create fun memories.

Ways To Buy Your Vacation Home

And you don’t have to be wealthy to buy a vacation home. Bankrate shares two tips for how to make this dream more achievable for anyone who’s interested:

Buy with loved ones or friends: If you’re okay with sharing the vacation home, you can go in on the purchase price together and pool your resources to make it more affordable.

Put a savings plan in place: This will require patience and persistence but consider adding a vacation home savings plan to your budget and contributing to it monthly.

Finding Your Dream Spot with a Little Help from an Agent

If the idea of basking in the sun at your very own vacation home sounds appealing, you might want to start looking now. Summer’s when everyone’s trying to buy their slice of paradise, so it’s best to start early.

Your first move is to team up with a real estate agent. They know all the ins and outs of the area you want to be in, and which homes you should look at. Plus, they can give you the lowdown on everything you need to know about having a second home and how it can benefit you. The same article from Bankrate says:

“Buying real estate in a new area — or even one you’ve vacationed in for many years — requires expert guidance. That makes it a good idea to work with an experienced local lender who specializes in loans for vacation homes and a local real estate professional. Local lenders and Realtors will understand the required rules and specifics for the area you are buying, and a local Realtor will know what properties are available.”

Bottom Line

If the idea of owning your own vacation home appeals to you, Let’s Chat.

If you’ve been looking for a home at the high end of your market, but haven’t found the right one, you may have put your search on hold. But according to recent data, now may be the time to jump back in. Here’s why.

There Are More Luxury Homes To Choose From

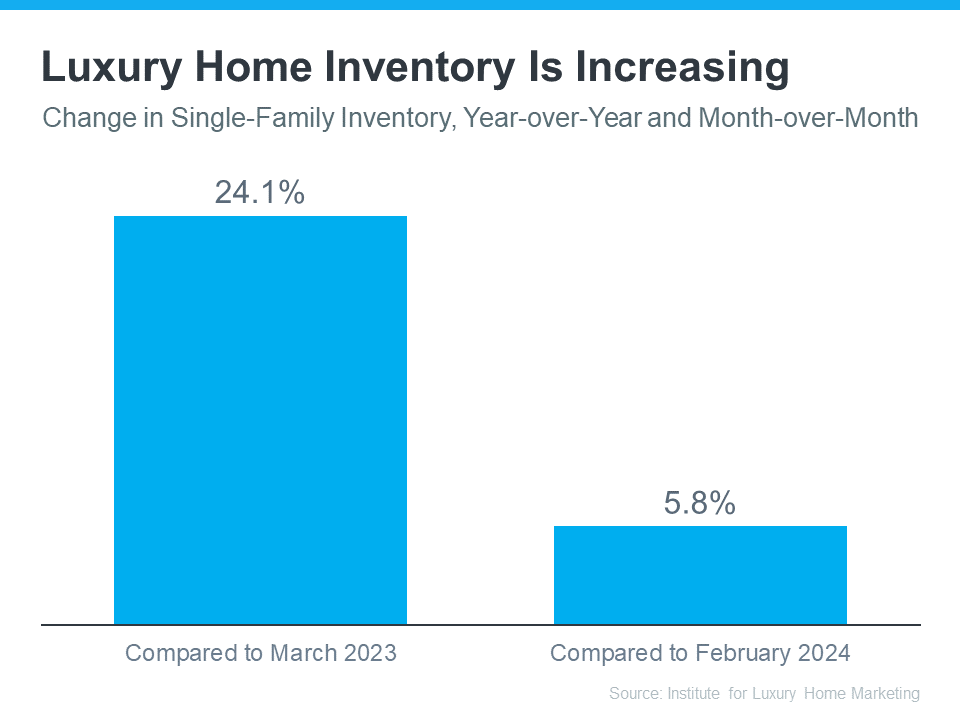

What’s considered the top-end of the market, or a luxury home, will always vary by location. But generally speaking, they’re homes that are valued in the top 5% of any given market. According to a recent report from the Institute forLuxury Home Marketing, the selection of luxury homes is increasing (see graph below):

As the graph shows, there are considerably more single-family luxury homes available now than there were a year ago. In fact, there are even more than there were just a month ago. This means you should have a wider variety of top-of-the-line homes to choose from, each with unique features and styles.

Whether you were searching for the latest design elements, like modern kitchens with chef-grade appliances, a breathtaking view, or integrated smart home technology, more luxury inventory means you should have an easier time finding one that matches your taste and lifestyle.

Rising Luxury Home Prices Can Help You Build Wealth

Another important factor to consider is that luxury home prices are on the rise. According to HousingWire, luxury home prices have increased by 8.7% over the past year. That’s why:

“People with the means to buy high-end homes are jumping in now because they feel confident prices will continue to rise . . . They’re ready to buy with more optimism and less apprehension.”

This means buying before prices climb higher – and while more inventory is on the market – may be your sweet spot. Because home prices are rising, owning a home could help you build more generational wealth over time. On the other hand, if you wait to buy, you might end up paying more for the same home later on as luxury prices continue to rise.

Bottom Line

With growing inventory and rising prices, you have a greater selection of luxury homes to choose from and an opportunity in front of you. Want to see the higher-end homes that are available in our area? Let’s connect today.

What To Expect if You Buy or Sell a Home This June

June is a busy month in the housing market because a lot of people buy and sell this time of year. So, if you’ve got a move on your mind and you’re looking to make it happen this month, here’s a snapshot of what you need to know to make sure you’re ready.

If You’re Buying This June

A lot of homebuyers with children like to move after one school year ends and before the next one begins. That’s one reason why late spring into summer is a popular time for homes to change hands. And whether that’s a motivator for you or not, it’s important to realize more buyers are going to be looking right now – and that means you’ll want to be ready for a bit more competition. But there is a silver lining to a move this time of year. This is also when more sellers will list – so you should find you have more options. As an article from Bankrate says:

“Late spring and early summer are the busiest and most competitive time of year for the real estate market. There’s usually more inventory listed for sale than other times of year . . . This is a double-edged sword for a buyer, as you will be met with more opportunities but [also] much more competition.”

During this busy season, it’s extra important to work with a trusted real estate agent. Your agent will help you stay on top of the latest listings, share expertise on how to make a strong offer in a competitive market, and give you insight into things like what the home is actually worth so you can make an informed decision when you buy. As Forbes says:

“Approaching the market confidently, armed with good information and grounded expectations will take you far. Don’t let the hustle of the market convince you to buy something that’s not in your budget, or not right for your lifestyle.”

If You’re Selling This June

Because there are more buyers this time of year, you’re in a great spot as a seller. Many of those buyers are highly motivated to make their move happen before the next school year kicks off – so they’ll likely put in strong offers to try to make that possible. That means, if your house shows well and is listed at market value, you could see your house sell faster or for a higher price. According to the National Association of Realtors (NAR):

“Warmer weather and the end of the school year encourage more people to buy and sell, respectively. Buyers are looking to move and settle before the new school year begins, contributing to increased competition and, consequently, higher prices.”

You want to be sure you’ve got a great agent on your side to help you with the contingencies on those offers and any negotiations that take place so you can pick the best offer. Make sure you go over closing dates with your agent. Buyers trying to time their move with the school year may need to delay a bit or move faster. This can depend on the school calendar where you live. As U.S. NewsReal Estate explains:

“ . . if your house goes under contract in early summer, the buyer may ask for a delay in closing or move-in until the school year finishes or their current home has sold. Alternatively, a buyer later in summer may be looking to close quickly and move in under a month. Remain flexible to keep the deal running smoothly, and your buyer may be willing to throw in concessions, like covering some of your closing costs or overlooking the old roof.”

Bottom Line

If you’re looking to make a move this June, let’s chat so you know what to expect. We’ll come up with a plan that factors in current market conditions, but still works for you.

For over 80 years, Veterans Affairs (VA) home loans have helped millions of veterans buy their own homes. If you or someone you know has served in the military, it’s important to learn about this program and its benefits.

Here are some key things to know about VA loans before buying a home.

Top Benefits of VA Home Loans

VA home loans make it easier for veterans to buy a home, and they’re a great perk for those who qualify. According to the Department of Veteran Affairs, some benefits include:

Options for No Down Payment: Qualified borrowers can often purchase a home with no down payment. That’s a huge weight lifted when you’re trying to save for a home. The Associated Presssays:

“. . . about 90% of VA loans are used to purchase a home with no money down.”

Don’t Require Private Mortgage Insurance (PMI): Many other loans with down payments under 20% require PMI. VA loans do not, which means veterans can save on their monthly housing costs.

Limited Closing Costs: There are limits on the types of closing costs you pay when you qualify for a VA home loan. So, more money stays in your pocket when it’s time to seal the deal.

An article from Veterans United sums up how remarkable this loan can be:

“For the vast majority of military borrowers, VA loans represent the most powerful lending program on the market. These flexible, $0-down payment mortgages have helped more than 24 million service members become homeowners since 1944.”

Bottom Line

Owning a home is the American Dream. Veterans give a lot to protect our country, and one way to honor them is by making sure they know about VA home loans.

Thinking about buying a home? While today’s mortgage rates might seem a bit intimidating, here are two solid reasons why, if you’re ready and able, it could still be a smart move to get your own place.

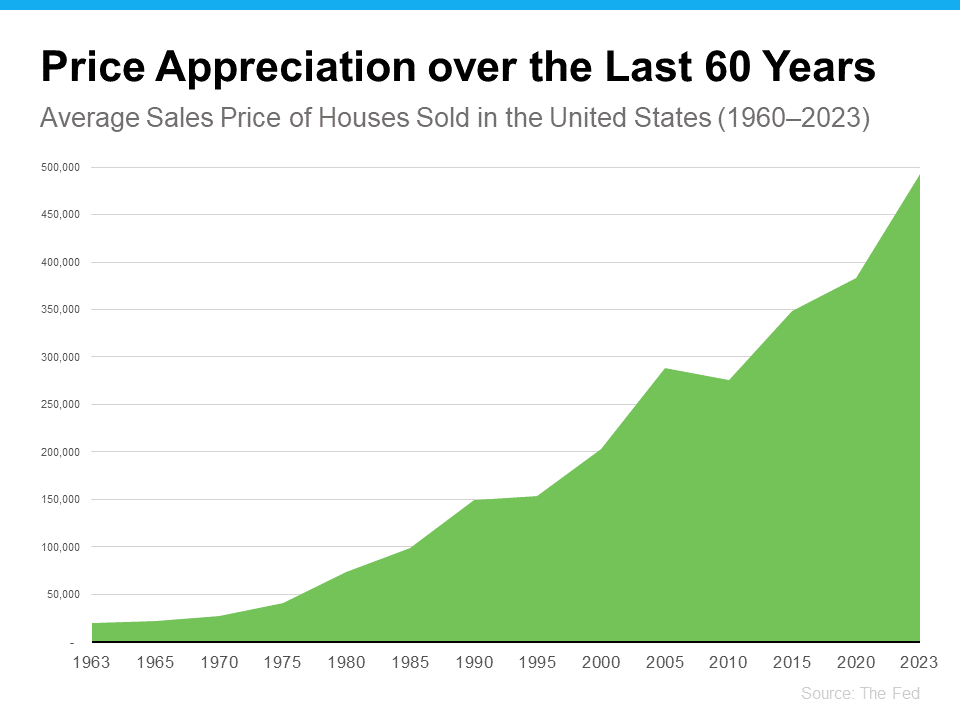

1. Home Values Typically Go Up Over Time

There’s been some confusion over the past year or so about which way home prices are headed. Make no mistake, nationally they’re still going up. In fact, over the long-term, home prices almost always go up (see graph below):

Using data from the Federal Reserve (the Fed), you can see the overall trend is home prices have climbed steadily for the past 60 years. There was an exception during the 2008 housing crash when prices didn’t follow the normal pattern, but generally, home values kept rising.

This is a big reason why buying a home can be better than renting. As prices go up and you pay down your mortgage, you build equity. Over time, this growing equity can really increase your net worth. The Urban Institutesays:

“Homeownership is critical for wealth building and financial stability.”

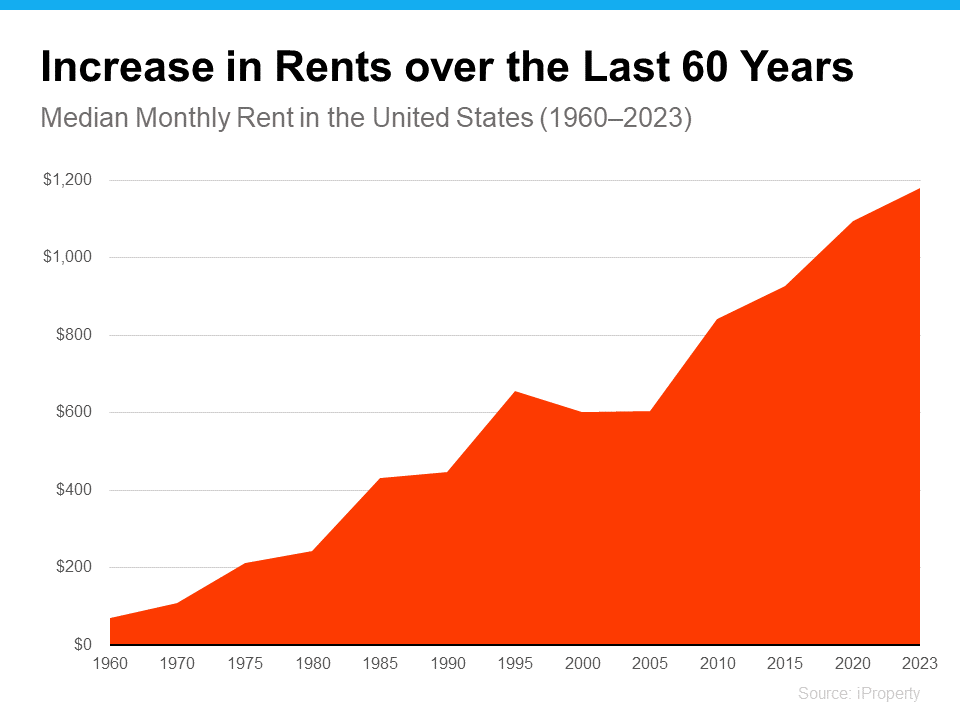

2. Rent Keeps Rising in the Long Run

Here’s another reason you may want to think about buying a home instead of renting – rent just keeps going up over the years. Sure, it might be cheaper to rent right now in some areas, but every time you renew your lease or sign a new one, you’re likely to feel the squeeze of your rent getting higher. According to data from iProperty Management, rent has been going up pretty consistently for the last 60 years, too (see graph below):

So how do you escape the cycle of rising rents? Buying a home with a fixed-rate mortgage helps you stabilize your housing costs and say goodbye to those annoying rent increases. That kind of stability is a big deal.

Your housing payments are like an investment, and you’ve got a decision to make. Do you want to invest in yourself or keep paying your landlord?

When you own your home, you’re investing in your own future. And even when renting is cheaper, that money you pay every month is gone for good.

As Dr. Jessica Lautz, Deputy Chief Economist and VP of Research at the National Association of Realtors (NAR), says:

“If a homebuyer is financially stable, able to manage monthly mortgage costs and can handle the associated household maintenance expenses, then it makes sense to purchase a home.”

Bottom Line

If you’re tired of your rent going up and want to explore the many benefits of homeownership, let’s talk to explore your options.

Over the past year or so, a lot of people have been talking about how tough it is to buy a home. And while there’s no arguing affordability is still tight, there are signs it’s starting to get a bit better and may improve even more throughout the year. Elijah de la Campa, Senior Economist at Redfin, says:

“We’re slowly climbing our way out of an affordability hole, but we have a long way to go. Rates have come down from their peak and are expected to fall again by the end of the year, which should make homebuying a little more affordable and incentivize buyers to come off the sidelines.”

Here’s a look at the latest data for the three biggest factors that affect home affordability: mortgage rates, home prices, and wages.

1. Mortgage Rates

Mortgage rates have been volatile this year – bouncing around in the upper 6% to low 7% range. That’s still quite a bit higher than where they were a couple of years ago. But there is a sliver of good news.

Despite the recent volatility, rates are still lower than they were last fall when they reached nearly 8%. On top of that, most experts still think they’ll come down some over the course of the year. A recent article from Bright MLSexplains:

“Expect rates to come down in the second half of 2024 but remain above 6% this year. Even a modest drop in rates will bring both more buyers and more sellers into the market.”

Any drop in rates can make a difference for you. When rates go down, you can afford the home you really want more easily because your monthly payment would be lower.

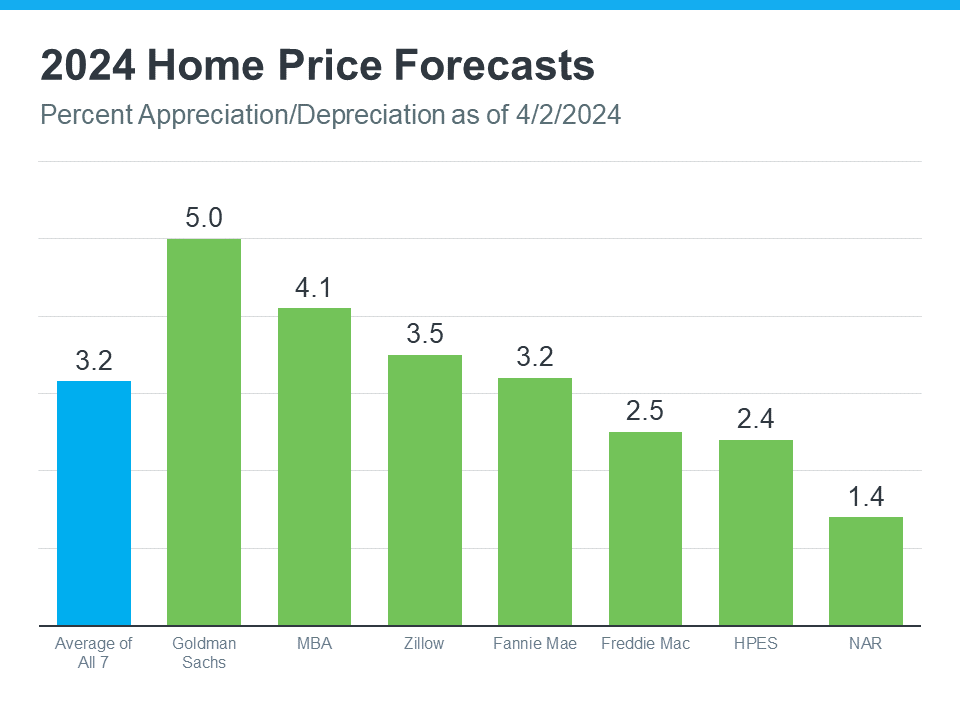

2. Home Prices

The second big factor to think about is home prices. Most experts project they’ll keep going up this year, but at a more normal pace. That’s because there are more homes on the market this year, but still not enough for everyone who wants to buy one. The graph below shows the latest 2024 home price forecasts from seven different organizations:

These forecasts are actually good news for you because it means the prices aren’t likely to shoot up sky high like they did during the pandemic. That doesn’t mean they’re going to fall – they’ll just rise at a slower pace.

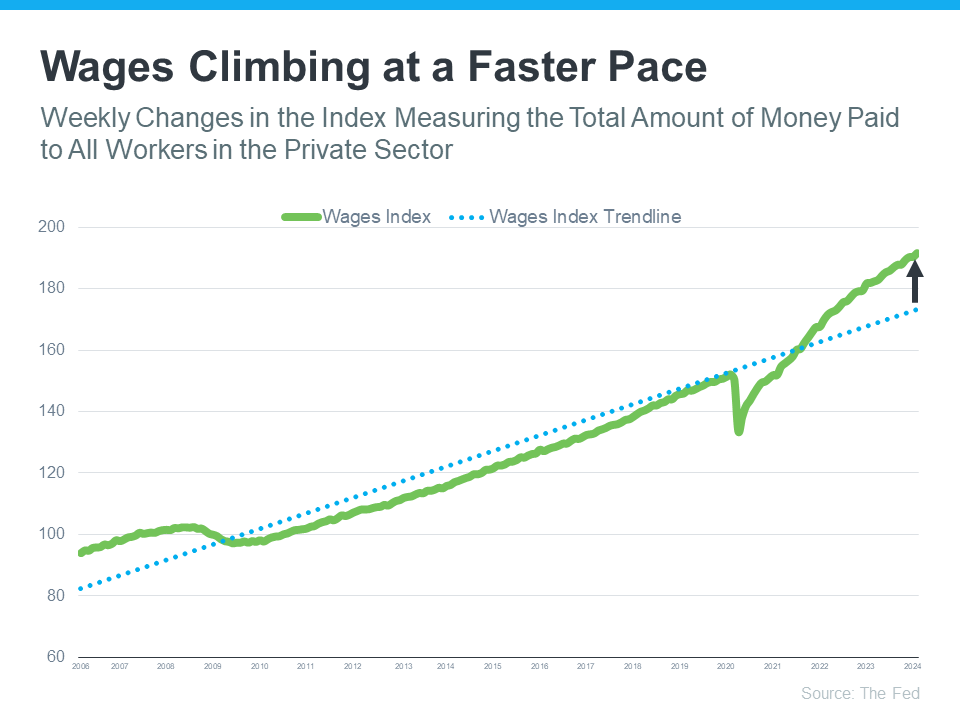

3. Wages

One factor helping affordability right now is the fact that wages are rising. The graph below uses data from the Federal Reserve to show how wages have been growing over time:

Check out the blue dotted line. That shows how wages typically rise. If you look at the right side of the graph, you’ll see wages are climbing even faster than normal right now.

Here’s how this helps you. If your income has increased, it’s easier to afford a home because you don’t have to spend as big of a percentage of your paycheck on your monthly mortgage payment.

Bottom Line

If you stack these factors up, you’ll see mortgage rates are still projected to come down a bit later this year, home prices are going up at a more moderate pace, and wages are growing quicker than normal. Those trends are a good sign for your ability to afford a home.

If you’re trying to sell your house, you may be looking at this spring season as the sweet spot – and you’re not wrong. We’re still in a seller’s market because there are so few homes for sale right now. And historically, this is the time of year when more buyers move, and competition ticks up. That makes this an exciting time to put up that for sale sign.

But while conditions are great for sellers like you, you’ll still want to be strategic when it comes time to set your asking price. That’s because pricing your house too high may actually cost you in the long run.

The Downside of Overpricing Your House

The asking price for your house sends a message to potential buyers. From the moment they see your listing, the price and the photos are what’s going to make the biggest first impression. And, if it’s priced too high, you may turn people away. As an article from U.S. News Real Estatesays:

“Even in a hot market where there are more buyers than houses available for sale, buyers aren’t going to pay attention to a home with an inflated asking price.”

That’s because no homebuyer wants to pay more than they have to, especially not today. Many are already feeling the pinch on their budget due to ongoing home price appreciation and today’s mortgage rates. And if they think your house is overpriced, they may write it off without even stepping foot in the front door, or simply won’t make an offer if they think it’s priced too high.

If that happens, it’s going to take longer to sell. And ideally you don’t want to have to think about doing a price drop to try to re-ignite interest in your house. Why? Some buyers will see the price cut as a red flag and wonder why the price was reduced, or they’ll think something is wrong with the house the longer it sits. As an article from Forbesexplains:

“It’s not only the price of an overpriced home that turns buyers off. There’s also another negative component that kicks in. . . . if your listing just sits there and accumulates days on the market, it will not be a good look. . . . buyers won’t necessarily ask anyone what’s wrong with the home. They’ll just assume that something is indeed wrong, and will skip over the property and view more recent listings.”

Your Agent’s Role in Setting the Right Price

Instead, pricing it at or just below current market value from the start is a much better strategy. So how do you find that ideal asking price? You lean on the pros. Only an agent has the expertise needed to research and figure out the current market value for your home.

They’ll factor in the condition of your house, any upgrades you’ve made, and what other houses like yours are selling for in your area. And they’ll use all of that information to find that target number. The right price will bring in more buyers and make it more likely you’ll see multiple offers too. Plus, when homes are priced right, they still tend to sell quickly.

Bottom Line

Even though you want to bring in top dollar when you sell, setting the asking price too high may deter buyers and slow down the sales process.

Let’s connect to find the right price for your house, so we can maximize your profit and still draw in eager buyers willing to make competitive offers.

Homeowners Today Have Options To Avoid Foreclosure

Even with the latest data coming in, the experts agree there’s no chance of a large-scale foreclosure crisis like the one we saw back in 2008. While headlines may be calling attention to a slight uptick in foreclosure filings recently, the bigger picture is that we’re still well below the number we’d see in a more normal year for the housing market. As a report from BlackKnightexplains:

“The prospect of any kind of near-term surge in foreclosure activity remains low, with start volumes still nearly 40% below pre-pandemic levels.”

That’s good news. It means the number of homeowners at risk is very low compared to the norm.

But, there’s a small percentage who may be coming face to face with foreclosure as a possibility. That’s because some homeowners may have an unexpected hardship in their life, which unfortunately can happen in any market.

For those homeowners, there are still options that could help them avoid having to go through the foreclosure process. If you’re facing difficulties yourself, an article from Bankrate breaks down some things to explore:

Look into Forbearance Programs: If you have a loan from Fannie Mae or Freddie Mac, you may be able to apply for this type of program.

Ask for a loan modification: Your lender may be willing to adjust your loan terms to help bring down your monthly payment to something more achievable.

Get a repayment plan in place: A lender may be able to set up a deferral or a payment plan if you’re not in a place where you’re able to make your payment.

And there’s something else you may want to consider. That’s whether you have enough equity in your home to sell it and protect your investment.

You May Be Able To Use Your Equity To Sell Your House

In today’s real estate market, many homeowners have far more equity in their homes than they realize due to the rapid home price appreciation we’ve seen over the past few years. That means, if you’ve lived in your house for a while, chances are your home’s value has gone up. Plus, the mortgage payments you’ve made during that time have chipped away at the balance of your loan. That combo may have given your equity a boost. And if your home’s current value is higher than what you still owe on your loan, you may be able to use that increase to your advantage. Freddie Macexplains how this can help:

“If you have enough equity, you can use the proceeds from the sale of your home to pay off your remaining mortgage debt, including any missed mortgage payments or other debts secured by your home.”

Lean on Experts To Explore Your Options

To find out how much equity you have, partner with a local real estate agent. They can give you an estimate of what your house could sell for based on recent sales of similar homes in your area. You may be able to sell your house to avoid foreclosure.

Bottom Line

If you’re a homeowner facing hardship, lean on a real estate professional to explore your options or see if you can sell your house to avoid foreclosure.

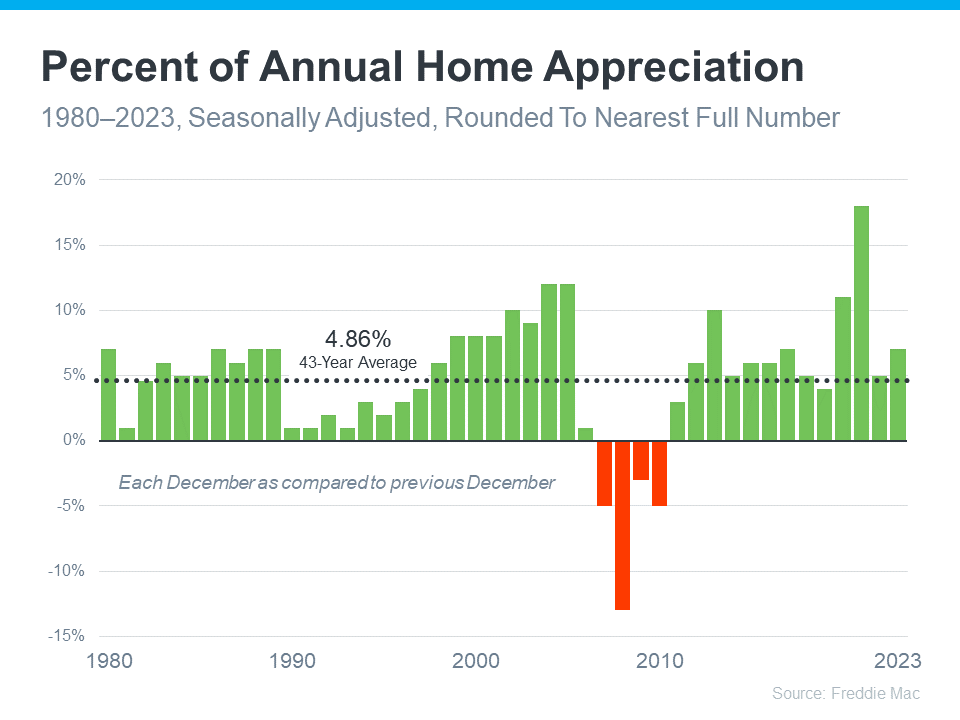

Going into 2023, there was a lot of talk about a possible recession that would cause the housing market to crash. Some in the media were even forecasting home prices would drop by as much as 10-20%—and that might have made you feel a bit unsure about buying a home.

But here’s what actually happened: home prices went up more than usual. Brian D. Luke, Head of Commodities at S&P Dow Jones Indices, explains:

“Looking back at the year, 2023 appears to have exceeded average annual home price gains over the past 35 years.”

To put last year’s growth into context, the graph below uses data from Freddie Mac on how home prices have changed each year going back to 1980. The dotted line shows the long-term average for appreciation:

“. . . the U.S. real estate market has a long and reliable history of increasing in value over time.”

In fact, since 1980, the only time home prices dropped was during the housing market crash (shown in red in the graph above). Fortunately, the market today isn’t like it was in 2008. For starters, there aren’t enough available homes to meet buyer demand right now. On top of that, homeowners have a tremendous amount of equity, so they’re on much stronger footing than they were back then. That means there won’t be a wave of foreclosures that causes prices to fall.

The fact that home values went up every single year except those four in red is why owning a home can be one of the smartest moves you can make. When you’re a homeowner, you own something that typically becomes more valuable over time. And as your home’s value appreciates, your net worth grows.

So, if you’re financially stable and prepared for the costs and expenses of homeownership, buying a home might make a lot of sense for you.

Bottom Line

Home prices almost always go up over time. That makes buying a home a smart move, if you’re ready and able. Let’s connect to talk about your goals and what’s available in our area.

Discover Luxury Living at Costa Blanca Condominiums with Keith Bailey, Your Expert Realtor

Nestled along the pristine shores of Florida’s famed Emerald Coast lies a hidden gem that epitomizes luxury coastal living – the Costa Blanca Condominiums. Located in the picturesque Santa Rosa Beach, these condominiums are more than just homes; they are a testament to elegance and refined living. This blog post, presented by Keith Bailey, a renowned realtor specializing in high-end properties, is your guide to discovering the opulent lifestyle that awaits at Costa Blanca.

The Allure of Santa Rosa Beach

Santa Rosa Beach is more than a destination; it’s a lifestyle. This enchanting locale, with its sugar-white sand and crystal-clear waters of the Gulf of Mexico, offers a serene retreat from the bustle of city life. It’s a place where the sun seems to shine a little brighter and the waves sing a more inviting tune.

A Haven for Nature Lovers and Adventurers: The natural scenery here is unmatched. From the dune lakes, unique to only a few places in the world, to the Point Washington State Forest, there’s an abundance of natural beauty to explore. Whether it’s paddle boarding, fishing, or simply soaking up the sun, the beach offers endless opportunities for relaxation and adventure.

Cultural Richness and Culinary Delights: Santa Rosa Beach is also a cultural hub with a thriving arts scene. The area boasts numerous art galleries, local craft shops, and seasonal festivals that celebrate the rich local heritage. Additionally, the culinary landscape is diverse, with everything from upscale dining to charming beachside shacks, serving fresh seafood and local delicacies.

Community Spirit and Accessibility: Despite its luxurious ambiance, Santa Rosa Beach exudes a warm community spirit. It’s a place where neighbors know each other and gather for community events. Furthermore, its proximity to airports and major cities makes it an accessible haven for both permanent residents and vacationers.

In this idyllic setting, Costa Blanca Condominiums stand as a beacon of luxury and comfort, harmonizing with the beauty and lifestyle of Santa Rosa Beach.

Spotlight on Costa Blanca Condominiums

Costa Blanca, a name synonymous with luxury and elegance, presents a living experience that is unparalleled in Santa Rosa Beach. These exclusive condominiums, with their stunning architecture and impeccable design, offer residents a slice of paradise along the tranquil shores of the Gulf of Mexico.

Architectural Excellence and Design Sophistication: Each condominium at Costa Blanca is a masterpiece, blending modern aesthetics with functional elegance. The buildings are designed to maximize the breathtaking views of the emerald waters and sandy beaches. High ceilings, spacious floor plans, and large windows create an ambiance of openness and luxury.

World-Class Amenities and Exclusive Features: Living at Costa Blanca means having access to a range of top-tier amenities. Residents enjoy private beach access, ensuring a serene beach experience any time. The state-of-the-art fitness center, heated outdoor pool, and lush landscaping add to the exclusivity. Security is paramount, with gated entry and 24-hour surveillance for peace of mind.

Variety and Personalization: Recognizing that each resident’s needs are unique, Costa Blanca offers a variety of floor plans. From intimate one-bedroom units to expansive multi-bedroom homes, each condo can be personalized to suit individual tastes and styles. The attention to detail in finishings and fixtures speaks volumes of the luxury that Costa Blanca upholds.

In essence, Costa Blanca isn’t just about luxurious homes; it’s about creating a lifestyle that resonates with elegance and tranquility, all while providing the comfort and convenience of modern living.

Lifestyle and Community at Costa Blanca

The lifestyle at Costa Blanca Condominiums is about more than just enjoying the breathtaking views and luxurious amenities; it’s about being part of a community that values quality, comfort, and a sense of belonging.

A Community of Like-Minded Individuals: Costa Blanca attracts a diverse group of residents, all united by a desire for a lifestyle that combines luxury with a sense of community. Here, neighbors are not just faces in the elevator but friends at social gatherings, beach outings, and community events.

Engagement and Activities: The community calendar at Costa Blanca is filled with various activities. From yoga classes on the beach to sunset gatherings, there’s always something happening. For those seeking a more relaxed pace, the serene environment offers the perfect backdrop for leisurely walks along the beach or quiet evenings on private balconies. Visit South Walton and Santa Rosa Beach

Privacy and Serenity: Despite its communal spirit, Costa Blanca also respects the privacy of its residents. The design of the condominiums and the layout of the complex ensure that everyone can enjoy their own space without intrusion. The tranquil surroundings further enhance the sense of peace and serenity.

Living at Costa Blanca is not just about the physical space; it’s about a lifestyle that promotes well-being, relaxation, and a sense of community. It’s a place where every day feels like a vacation.

Why Choose Keith Bailey as Your Realtor

When considering a property as exclusive as Costa Blanca Condominiums, partnering with the right realtor is crucial. Keith Bailey stands out as a real estate expert, especially in the luxury market of Santa Rosa Beach.

Experience and Expertise: With years of experience in the luxury real estate market, Keith has an in-depth understanding of what makes a property like Costa Blanca so special. His knowledge of the local market dynamics, property values, and investment potential makes him an invaluable asset to potential buyers.

Personalized Service and Attention to Detail: Keith is known for his personalized approach to real estate. He takes the time to understand his clients’ unique needs and preferences, ensuring that every property viewing and transaction is tailored to meet those specific requirements. View All Santa Rosa Beach Properties For Sale

Success Stories and Client Satisfaction: Keith’s track record speaks for itself. He has successfully guided numerous clients through the process of finding their dream home or investment property. Testimonials from satisfied clients highlight his professionalism, dedication, and ability to close deals that exceed expectations.

A Trusted Advisor and Negotiator: In the competitive market of high-end real estate, having a skilled negotiator like Keith is essential. He not only advocates for his clients’ best interests but also ensures a smooth and stress-free transaction process.

Choosing Keith Bailey as your realtor means partnering with someone who is not just an agent but a trusted advisor, committed to finding you the perfect home at Costa Blanca Condominiums.

What To Know About Credit Scores Before Buying a Home

If you want to buy a home, you should know your credit score is a critical piece of the puzzle when it comes to qualifying for a mortgage. Lenders review your credit to see if you typically make payments on time, pay back debts, and more. Your credit score can also help determine your mortgage rate. An article from US Bankexplains:

“A credit score isn’t the only deciding factor on your mortgage application, but it’s a significant one. So, when you’re house shopping, it’s important to know where your credit stands and how to use it to get the best mortgage rate possible.”

That means your credit score may feel even more important to your homebuying plans right now since mortgage rates are a key factor in affordability. According to the Federal Reserve Bank of New York, the median credit score in the U.S. for those taking out a mortgage is 770. But that doesn’t mean your credit score has to be perfect. The same article from US Bankexplains:

“Your credit score (commonly called a FICO Score) can range from 300 at the low end to 850 at the high end. A score of 740 or above is generally considered very good, but you don’t need that score or above to buy a home.”

Working with a trusted lender is the best way to get more information on how your credit score could factor into your home loan and the mortgage rate you’re able to get. As FICOsays:

“While many lenders use credit scores like FICO Scores to help them make lending decisions, each lender has its own strategy, including the level of risk it finds acceptable. There is no single “cutoff score” used by all lenders and there are many additional factors that lenders may use to determine your actual interest rates.”

If you’re looking for ways to improve your score, Experianhighlights some things you may want to focus on:

Your Payment History: Late payments can have a negative impact by dropping your score. Focus on making payments on time and paying any existing late charges quickly.

Your Debt Amount (relative to your credit limits): When it comes to your available credit amount, the less you’re using, the better. Focus on keeping this number as low as possible.

Credit Applications: If you’re looking to buy something, don’t apply for additional credit. When you apply for new credit, it could result in a hard inquiry on your credit that drops your score.

Bottom Line

Finding ways to make your credit score better could help you get a lower mortgage rate. If you want to learn more, talk to a trusted lender.

Buying your first home is a big, exciting step and a major milestone that has the power to improve your life. As a first-time homebuyer, it’s a dream you can make come true, but there are some hurdles you’ll need to overcome in today’s housing market – specifically the limited supply of homes for sale and ongoing affordability challenges.

So, if you’re ready, willing, and able to buy your first home, here are three tips to help you turn your dream into a reality.

Save Money with First-Time Homebuyer Programs

Paying the initial costs of homeownership, like your down payment and closing costs, can feel a bit daunting. But there are many assistance programs for first-time homebuyers that can help you get a loan with little or no money upfront. According to Bankrate:

“. . . you might qualify for a first-time homebuyer loan or assistance. First-time buyer loans typically have more flexible requirements, such as a lower down payment and credit score. Many help buyers with closing costs and the down payment through grants and low-interest loans.”

To find out more, talk to your state’s housing authority or check out websites like Down Payment Resource.

Expand Your Options by Looking at Condos and Townhomes

Right now, there aren’t enough homes for sale for everyone who wants to buy one. That’s pushing home prices up and making affordability tight for buyers. One way to deal with that issue and find a home right now is to consider condos and townhomes. Realtor.comexplains:

“For many newbies, it might just be a matter of making a shift toward something they can better afford—like a condo or townhome. These lower-cost homes have historically been a stepping stone for buyers looking for a less expensive alternative to a single-family home.”

One reason why they may be more affordable is because they’re often smaller. But they still give you the chance to get your foot in the door and achieve your goal of owning a home and building equity. And that equity can help fuel your move into a larger home later on if you decide you need something bigger in the future. Hannah Jones, Senior Economic Analyst at Realtor.com, says:

“Condos can help prospective homebuyers who perhaps have a smaller budget, but who are really determined to get a foothold in the market and start to accumulate some equity. It can be a really great entry point.”

Consider Pooling Your Resources To Buy a Multi-Generational Home

Another way to break into the market is by purchasing a home with friends or loved ones. That way you can split the cost of things like the mortgage and bills, to make it easier to afford a home. According to Money.com:

“Buying a home with another person has some obvious advantages in the mortgage department. With two incomes in the mix, buyers can likely qualify for a larger mortgage — a big help in today’s high-cost market.”

Bottom Line

By exploring first-time homebuyer assistance, condos, townhomes, and multi-generational living, it can be easier to find and buy your first home. When you’re ready, let’s connect.

Don’t Let the Latest Home Price Headlines Confuse You

Based on what you’re hearing in the news about home prices, you may be worried they’re falling. But here’s the thing. The headlines aren’t giving you the full picture.

If you look at the national data for 2023, home prices actually showed positive growth for the year. While this varies by market, and while there were some months with slight declines nationally, those were the exception, not the rule.

The overarching story is that prices went up last year, not down. Let’s dive into the data to set the record straight.

2023 Was the Return to More Normal Home Price Growth

If anything, last year marked a return to more normal home price appreciation. To prove it, here’s what usually happens in residential real estate.

In the housing market, there are predictable ebbs and flows that take place each year. It’s called seasonality. It goes like this. Spring is the peak homebuying season when the market is most active. That activity is usually still strong in the summer, but begins to wane toward the end of the year. Home prices follow along with this seasonality because prices grow the most when there’s high demand.

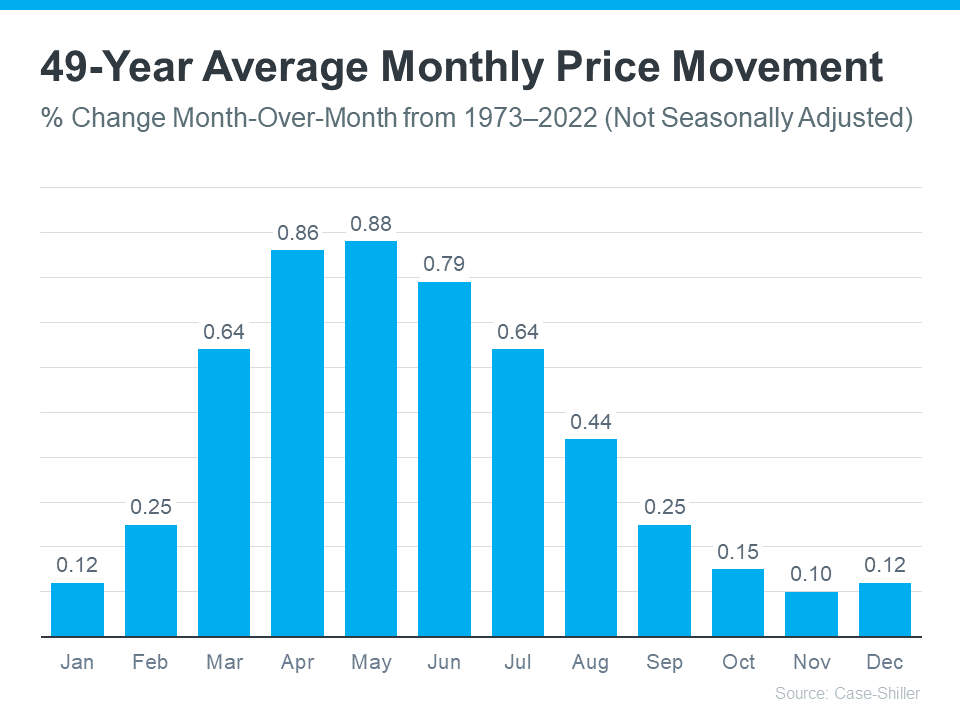

The graph below uses data from Case-Shiller to show how this pattern played out in home prices from 1973 through 2022 (not adjusted, so you can see the seasonality):

As the data shows, for nearly 50 years, home prices match typical market seasonality. At the beginning of the year, home prices grow more moderately. That’s because the market is less active as fewer people move in January and February. Then, as the market transitions into the peak homebuying season in the spring, activity ramps up. That means home prices do too. Then, as fall and winter approach, activity eases again and prices grow, just at a slower rate.

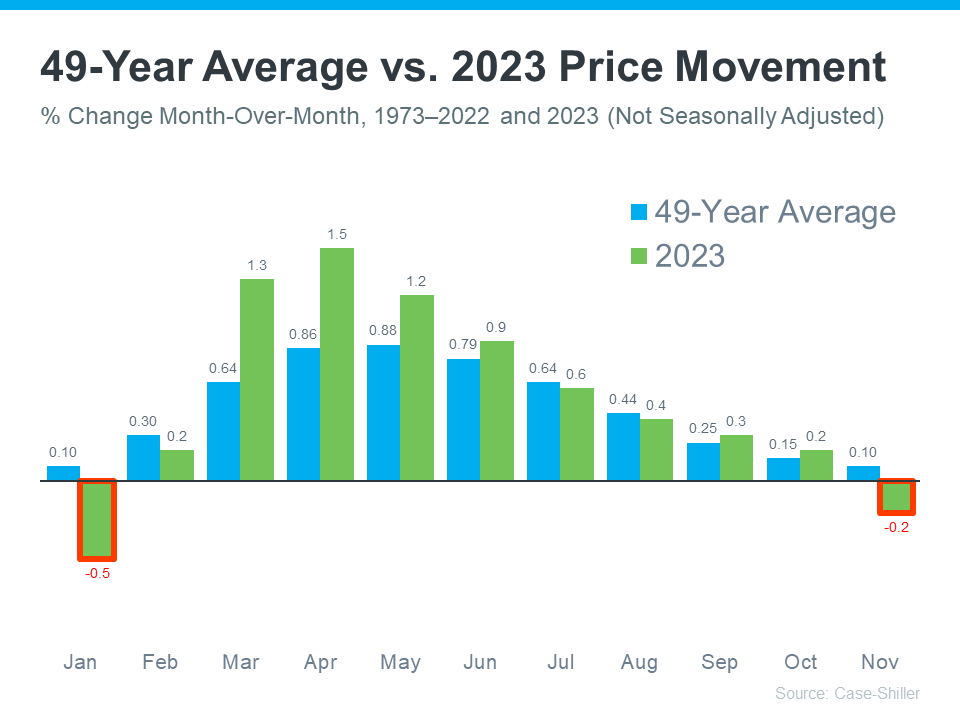

Now, let’s layer the data that’s come out for 2023 so far (shown in green) on top of that long-term trend (still shown in blue). That way, it’s easy to see how 2023 compares.

As the graph shows, moving through the year in 2023, the level of appreciation fell more in line with the long-term trend for what usually happens in the housing market. You can see that in how close the green bars come to matching the blue bars in the later part of the year.

But the headlines only really focused on the two bars outlined in red. Here’s the context you may not have gotten that can really put those two bars into perspective. The long-term trend shows it’s normal for home prices to moderate in the fall and winter. That’s typical seasonality.

And since the 49-year average is so close to zero during those months (0.10%), that also means it’s not unusual for home prices to drop ever so slightly during those times. But those are just blips on the radar. If you look at the year as a whole, home prices still rose overall.

What You Really Need To Know

Headlines are going to call attention to the small month-to-month dips instead of the bigger year-long picture. And that can be a bit misleading because it’s only focused on one part of the whole story.

Instead, remember last year we saw the return of seasonality in the housing market – and that’s a good thing after home prices skyrocketed unsustainably during the ‘unicorn’ years of the pandemic.

And just in case you’re still worried home prices will fall, don’t be. The expectation for this year is that prices will continue to appreciate as buyers re-enter the market due to mortgage rates trending down compared to last year. As buyer demand goes up and more people move at the same time the supply of homes for sale is still low, the upward pressure on prices will continue.

Bottom Line

Don’t let home price headlines confuse you. The data shows that, as a whole, home prices rose in 2023. If you have questions about what you’re hearing in the news or about what’s happening with home prices in our local area, let’s connect.

Are you on the fence about selling your house? While affordability is improving this year, it’s still tight. And that may be on your mind. But understanding your home equity could be the key to making your decision easier. An article from Bankrateexplains:

“Home equity is the difference between your home’s value and the amount you still owe on your mortgage. It represents the paid-off portion of your home.

You’ll start off with a certain level of equity when you make your down payment to buy the home, then continue to build equity as you pay down your mortgage. You’ll also build equity over time as your home’s value increases.”

Think of equity as a simple math equation. It’s the value of your home now minus what you owe on your mortgage. And guess what? Recently, your equity has probably grown more than you think.

In the past few years, home prices skyrocketed, which means your home’s value – and your equity – likely shot up, too. So, you may have more equity than you realize.

How To Make the Most of Your Home Equity Right Now

If you’re thinking about moving, the equity you have in your home could be a big help. According to CoreLogic:

“. . . the average U.S. homeowner with a mortgage still has more than $300,000 in equity . . .”

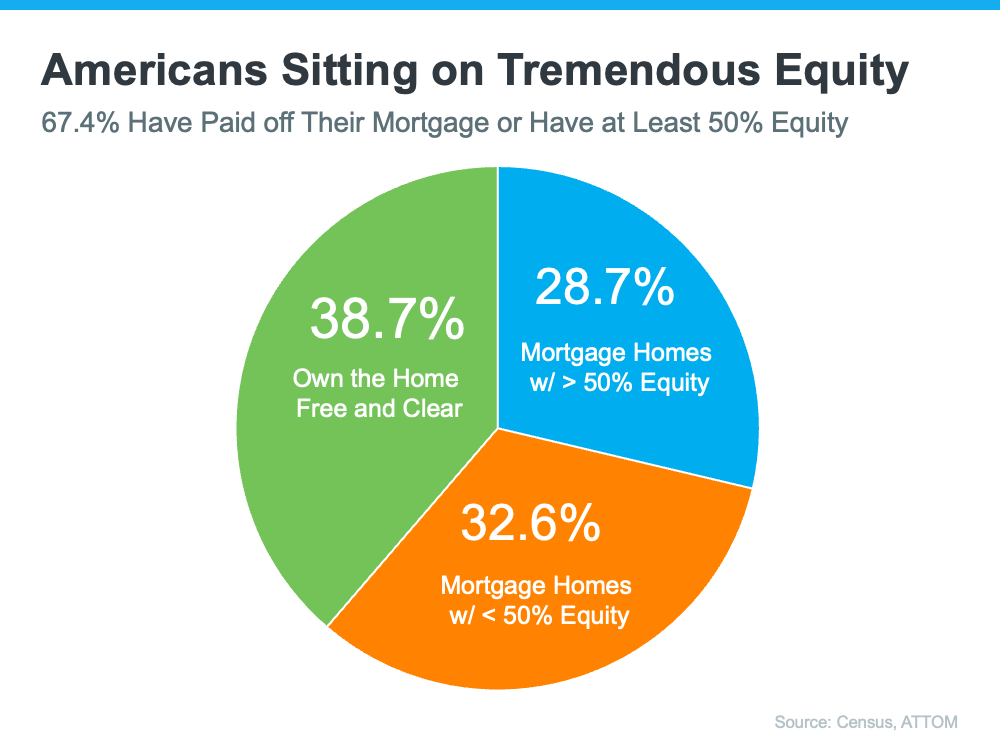

Clearly, homeowners have a lot of equity right now. And the latest data from the Census and ATTOM shows over two-thirds of homeowners have either completely paid off their mortgages (shown ingreen in the chart below) or have at least 50% equity (shown inblue in the chart below):

That means roughly 70% have a tremendous amount of equity right now.

Be an all-cash buyer: If you’ve been living in your current home for a long time, you might have enough equity to buy your next home without having to take out a loan. If that’s the case, you won’t need to borrow any money or worry about mortgage rates. Investopediastates:

“You may want to pay cash for your home if you’re shopping in a competitive housing market, or if you’d like to save money on mortgage interest. It could help you close a deal and beat out other buyers.”

Make a larger down payment: Your equity could also be used toward your next down payment. It might even be enough to let you put a larger amount down, so you won’t have to borrow as much money. The Mortgage Reportsexplains:

“Borrowers who put down more money typically receive better interest rates from lenders. This is due to the fact that a larger down payment lowers the lender’s risk because the borrower has more equity in the home from the beginning.”

The Easy Way To Find Out How Much Equity You Have

To find out how much equity you have in your home, ask a real estate agent you trust for a Professional Equity Assessment Report (PEAR).

Bottom Line

Planning a move? Your home equity can really help you out. Let’s connect to see how much equity you have and how it can help with your next home.

Contact Keith Bailey Realtor at 850-830-6771 or Contact here

On the road to becoming a homeowner? If so, you may have heard the term pre-approval get tossed around. Let’s break down what it is and why it’s important if you’re looking to buy a home in 2024.

What Pre-Approval Is

As part of the homebuying process, your lender will look at your finances to figure out what they’re willing to loan you. According to Investopedia, this includes things like your W-2, tax returns, credit score, bank statements, and more.

From there, they’ll give you a pre-approval letter to help you understand how much money you can borrow. Freddie Macexplains it like this:

“A pre-approval is an indication from your lender that they are willing to lend you a certain amount of money to buy your future home. . . . Keep in mind that the loan amount in the pre-approval letter is the lender’s maximum offer. Ultimately, you should only borrow an amount you are comfortable repaying.”

Now, that last piece is especially important. While home affordability is getting better, it’s still tight. So, getting a good idea of what you can borrow can help you really wrap your head around the financial side of things. It doesn’t mean you should borrow the full amount. It just tells you what you can borrow from that lender.

This sets you up to make an informed decision about your numbers. That way you’re able to tailor your home search to what you’re actually comfortable with budget-wise and can act fast when you find a home you love.

Why Pre-Approval Is So Important in 2024

If you want to buy a home this year, there’s another reason you’re going to want to be sure you’re working with a trusted lender to make this a priority.

While more homes are being listed for sale, the overall number of available homes is still below the norm. At the same time, the recent downward trend in mortgage rates compared to last year is bringing more buyers back into the market. That imbalance of more demand than supply creates a bit of a tug-of-war for you.

It means you’ll likely find you have more competition from other buyers as more and more people who were sitting on the sidelines when mortgage rates were higher decide to jump back in. But pre-approval can help with that too.

Pre-approval shows sellers you mean business because you’ve already undergone a credit and financial check. As Greg McBride, Chief Financial Analyst at Bankrate,says:

“Preapproval carries more weight because it means lenders have actually done more than a cursory review of your credit and your finances, but have instead reviewed your pay stubs, tax returns and bank statements. A preapproval means you’ve cleared the hurdles necessary to be approved for a mortgage up to a certain dollar amount.”

Sellers love that because that makes it more likely the sale will move forward without unexpected delays or issues. And if you may be competing with another buyer to land your dream home, why wouldn’t you do this to help stack the deck in your favor?

Bottom Line

If you’re looking to buy a home in 2024, know that getting pre-approved is going to be a key piece of the puzzle. With lower mortgage rates bringing more buyers back into the market, this can help you make a strong offer that stands out from the crowd.

Contact Keith Bailey Realtor 850-830-6771 OR Contact Me

Have you seen headlines talking about the increase in foreclosures in today’s housing market? If so, they may leave you feeling a bit uneasy about what’s ahead. But remember, these clickbait titles don’t always give you the full story.

The truth is, if you compare the current numbers with what usually happens in the market, you’ll see there’s no need to worry.

Putting the Headlines into Perspective

The increase the media is calling attention to is misleading. That’s because they’re only comparing the most recent numbers to a time where foreclosures were at historic lows. And that’s making it sound like a bigger deal than it is.

In 2020 and 2021, the moratorium and forbearance program helped millions of homeowners stay in their homes, allowing them to get back on their feet during a very challenging period.

When the moratorium came to an end, there was an expected rise in foreclosures. But just because foreclosures are up doesn’t mean the housing market is in trouble.

Historical Data Shows There Isn’t a Wave of Foreclosures

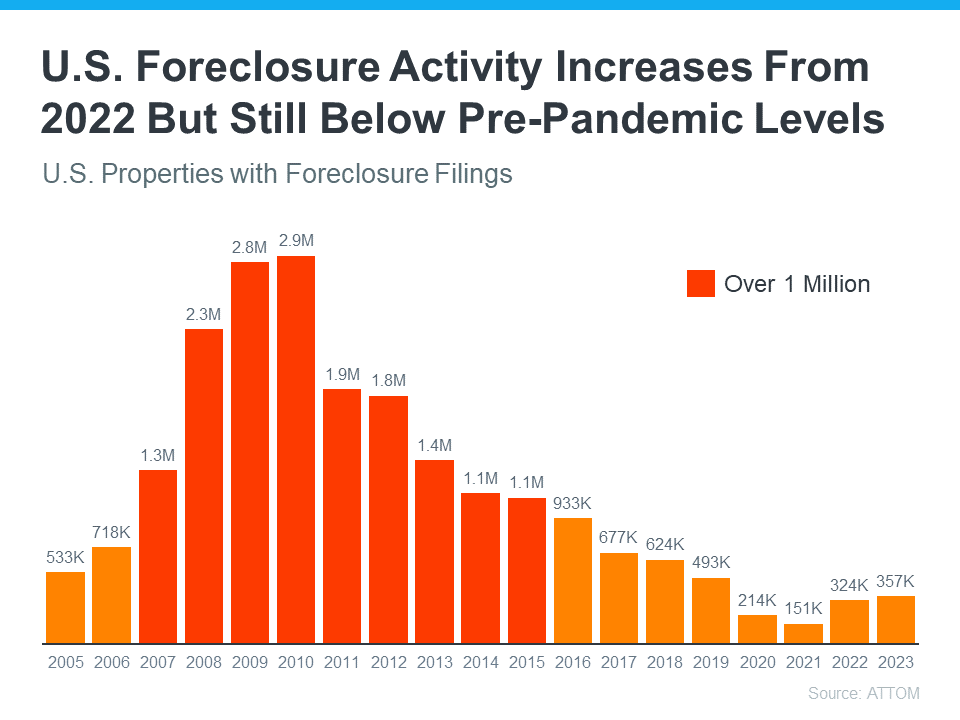

Instead of comparing today’s numbers with the last few abnormal years, it’s better to compare to long-term trends – specifically to the housing crash – since that’s what people worry may happen again.

Take a look at the graph below. It uses foreclosure data from ATTOM, a property data provider, to show foreclosure activity has been consistently lower (shown in orange) since the crash in 2008 (shown in red):

So, while foreclosure filings are up in the latest report, it’s clear this is nothing like it was back then.

In fact, we’re not even back at the levels we’d see in more normal years, like 2019. As Rick Sharga, Founder and CEO of the CJ Patrick Company, explains:

“Foreclosure activity is still only at about 60% of pre-pandemic levels. . .”

That’s largely because buyers today are more qualified and less likely to default on their loans. Delinquency rates are still low and most homeowners have enough equity to keep them from going into foreclosure. As Molly Boesel, Principal Economist at CoreLogic, says:

“U.S. mortgage delinquency rates remained healthy in October, with the overall delinquency rate unchanged from a year earlier and the serious delinquency rate remaining at a historic low… borrowers in later stages of delinquencies are finding alternatives to defaulting on their home loans.”

The reality is, while increasing, the data shows a foreclosure crisis is not where the market is today, or where it’s headed.

Bottom Line

Even though the housing market is experiencing an expected rise in foreclosures, it’s nowhere near the crisis levels seen when the housing bubble burst. If you have questions about what you’re hearing or reading about the housing market, let’s connect.

Contact Keith Bailey Realtor 850-830-6771 or Web Contact

If you’re looking to buy a home, you’ve probably been paying close attention to mortgage rates. Over the last couple of years, they hit record lows, rose dramatically, and are now dropping back down a bit. Ever wonder why?

The answer is complicated because there’s a lot that can influence mortgage rates. Here are just a few of the most impactful factors at play.

Inflation and the Federal Reserve

The Federal Reserve (Fed) doesn’t directly determine mortgage rates. But the Fed does move the Federal Funds Rate up or down in response to what’s happening with inflation, the economy, employment rates, and more. As that happens, mortgage rates tend to respond. Business Insider explains:

“The Federal Reserve slows inflation by raising the federal funds rate, which can indirectly impact mortgages. High inflation and investor expectations of more Fed rate hikes can push mortgage rates up. If investors believe the Fed may cut rates and inflation is decelerating, mortgage rates will typically trend down.”

Over the last couple of years, the Fed raised the Federal Fund Rate to try to fight inflation and, as that happened, mortgage rates jumped up, too. Fortunately, the expert outlook for inflation and mortgage rates is that both should become more favorable over the course of the year. As Danielle Hale, Chief Economist at Realtor.com, says:

“[M]ortgage rates will continue to ease in 2024 as inflation improves . . .”

There’s even talk the Fed may actually cut the Fed Funds Rate this year because inflation is cooling, even though it’s not yet back to their ideal target.

The 10-Year Treasury Yield

Additionally, mortgage companies look at the 10-Year Treasury Yield to decide how much interest to charge on home loans. If the yield goes up, mortgage rates usually go up, too. The opposite is also true. According to Investopedia:

“One frequently used government bond benchmark to which mortgage lenders often peg their interest rates is the 10-year Treasury bond yield.”

Historically, the spread between the 10-Year Treasury Yield and the 30-year fixed mortgage rate has been fairly consistent, but that’s not the case recently. That means, there’s room for mortgage rates to come down. So, keeping an eye on which way the treasury yield is trending can give experts an idea of where mortgage rates may head next.

Bottom Line

With the Fed meeting later this week, experts in the industry will be keeping a close watch to see what they decide and what impact it’ll have on the economy. To navigate any mortgage rate changes and their impact on your moving plans, it’s best to have a team of professionals on your side.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.

Here’s what that means. Five out of every six homes are being purchased by everyday homebuyers like you – not big investors.